A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Do Industrial Policies Improve Efficiency? Evidence From China's Credit Policies

Are industrial policies distorting the economy, or correcting underlying distortions? Using Chinese firm-level data and a quantitative model, this article shows that preferential credit is directed toward high-markup (high-return) sectors, reallocating resources toward underfunded activities. While such policies weaken firm selection, they improve aggregate efficiency: removing them would nearly double productivity losses. The results suggest that, in a second-best environment, well-targeted industrial policies can enhance rather than reduce overall efficiency.

Are industrial policies distorting the economy, or correcting underlying distortions?

This question has become increasingly relevant in light of China’s rapid rise in sectors such as electric vehicles, solar panels, and batteries—industries that have received substantial policy support. Traditional economic thinking tends to view such interventions as distortionary. But recent developments suggest a more nuanced picture.

A growing body of research shows that industrial policy can have powerful effects within specific sectors. For example, Barwick, Kalouptsidi, and Zahur (2024) document how policy support contributed to the rapid expansion and global competitiveness of China’s electric vehicle industry, while related work on shipbuilding (Barwick, Kalouptsidi, and Zahur 2025) shows how targeted subsidies reshaped industry structure and international market shares. On the other hand, recent studies by Fang, Li and Lu (2025) and Chang and Xiong (2026) find industry-wide overcapacity as potential downsides of industrial policies or credit expansion.

At the same time, a separate macroeconomic literature emphasizes that China’s economy is characterized by substantial distortions in credit allocation (e.g. Song, Storesletten, and Zilibotti 2011; Chang, Chen, Waggoner and Zha, 2016). Capital is not always directed to its highest-return uses, suggesting that the economy may already be far from an efficient benchmark. Put differently, the economy may already be distorted, before policy even enters the picture.

This brings us to the central question: can industrial policy improve efficiency by correcting these underlying distortions?

A recent paper in the Journal of International Economics (Chen, Huang, Liu, Lu and Wang, 2026) offers a new answer. Using firm-level data from China over 2009–2020 and a quantitative multi-sector model, the study shows that preferential credit policies can increase aggregate productivity and welfare by improving resource allocation across sectors.

How does credit policy affect resource allocation?

To see the mechanism, start from a simple observation: not all sectors in the economy generate the same returns to capital. In some industries—often those with stronger market power or technological advantages—firms can charge higher prices relative to their costs, which translates into higher returns on capital. If capital were perfectly allocated, more resources would flow into these high-return sectors until returns are equalized across the economy. But in practice, this does not fully happen. As a result, some sectors remain underfunded relative to their economic potential, while others receive too much capital.

This is where credit policy enters. By lowering financing costs in selected sectors, preferential credit can tilt the allocation of capital toward these high-return activities. In that sense, policy does not simply distort the market; rather it can partially correct an existing imbalance, reallocating resources toward sectors where the marginal return is higher. From this perspective, credit policy acts as a “rebalancing” force in an economy where market outcomes are already shaped by uneven competitive conditions.

At the same time, this reallocation comes with an important trade-off. Lower financing costs do not only benefit productive firms—they also make it easier for less efficient firms to survive. This weakens the market’s selection mechanism and can lead to the persistence of low-productivity, or “zombie,” firms. The overall effect of policy therefore depends on the balance between two forces: improved allocation across sectors versus weaker selection within sectors.

The contribution of the paper is to quantify this trade-off. It combines firm-level evidence with a structural model to measure how much efficiency is gained from reallocating capital toward high-return sectors, and how much is lost from reduced firm turnover. This framework makes it possible to assess whether preferential credit policies, on net, improve or reduce aggregate efficiency.

Evidence from China

Do these mechanisms show up in the data? The answer is yes. Using firm-level tax survey database from China over 2009–2020, the paper documents three key empirical patterns that align closely with the mechanism described above.

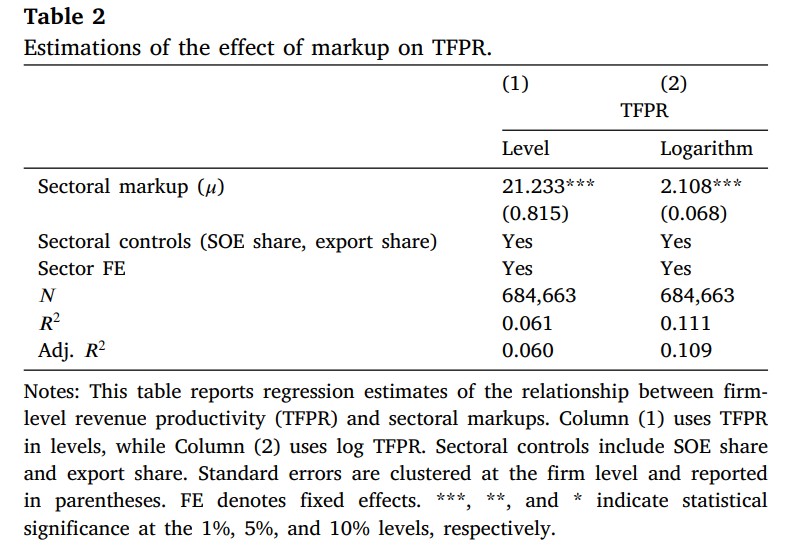

First, sectors with higher profit margins also exhibit higher revenue-based productivity, indicating that these sectors are under-resourced rather than over-expanded. In other words, capital is not flowing sufficiently toward the sectors where its marginal revenue product is highest.

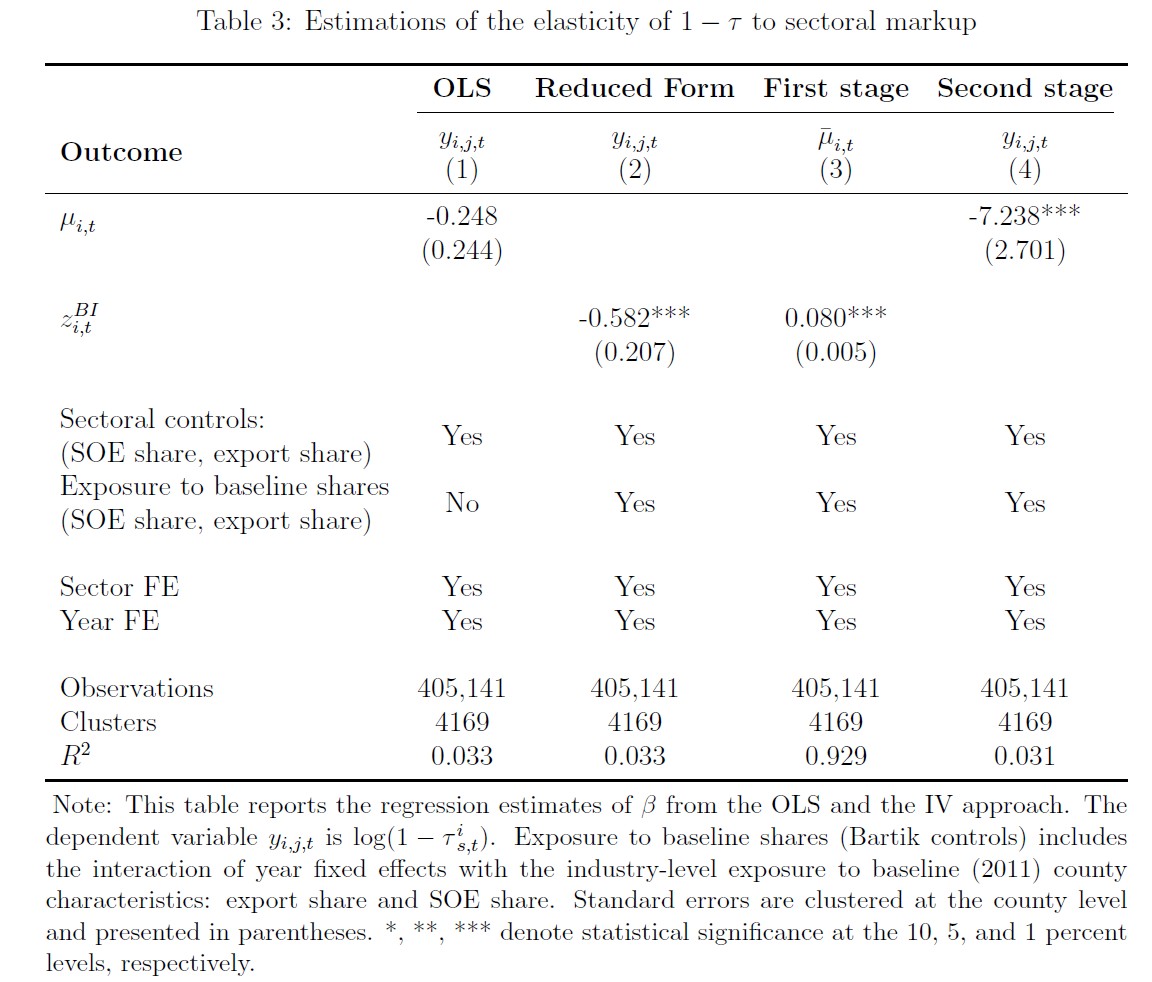

Second, preferential credit is disproportionately directed toward these high markup sectors. To establish this relationship, the paper uses a Bartik-style instrumental variable strategy that isolates the causal effects of sectoral markups on firm-level credit subsidy. The results show that sectors with higher markups face significantly lower effective financing costs. This suggests that credit policy is not randomly allocated, but systematically aligned with sectoral characteristics, such as future profitability and economic returns.

Third, this reallocation comes with a cost: credit subsidies increase the prevalence of zombie firms. Lower financing costs reduce the pressure for inefficient firms to exit, leading to a higher share of so-called “zombie” firms in more heavily subsidized sectors.

Taken together, these findings paint a coherent picture. Preferential credit policies simultaneously redirect resources toward high markup sectors and weaken firm-level selection. The key question, then, is whether the gains from improved allocation outweigh the costs from reduced efficiency within sectors—a question that requires a quantitative framework to answer.

Do the benefits outweigh the costs? Quantitative results

To assess the overall impact of credit policy, the paper brings together the empirical patterns and the mechanism in a quantitative multi-sector model calibrated to match the Chinese data. This allows the analysis to move beyond partial evidence and evaluate the net effect on aggregate efficiency.

The headline result is striking. If preferential credit policies were eliminated, aggregate productivity losses in manufacturing would increase from about 2.9% to 5.5%—nearly doubling the efficiency loss. In welfare terms, this corresponds to a decline of roughly 2.6%. In other words, despite the distortions it introduces, preferential credit improves overall economic outcomes.

Why does this happen? The answer lies in the balance between the two forces highlighted earlier. On the one hand, credit policy reallocates capital toward high-return sectors, generating large gains in allocative efficiency. On the other hand, it weakens firm selection, allowing less productive firms to remain in operation. The quantitative analysis shows that the first effect dominates. The gains from improved allocation substantially outweigh the losses from weaker selection. Moreover, lower financing costs also encourage firm entry, which further contributes to productivity by expanding the set of active producers.

Taken together, these results suggest that preferential credit policy operates as a second-best tool: while it introduces distortions at the firm level, it can still improve aggregate efficiency by correcting larger distortions across sectors.

Implications for industrial policy

What do these findings imply for how we think about industrial policy?

A first lesson is that policy should be evaluated relative to the distortions already present in the economy, not against an idealized benchmark of perfectly functioning markets. In a setting where capital is not allocated to its highest-return uses, interventions that appear distortionary in isolation may in fact improve overall efficiency by offsetting existing imbalances.

A second lesson is that the direction of policy matters more than the mere presence of policy. Preferential credit can be beneficial when it channels resources toward sectors with high marginal returns. But if credit is directed toward low-return or declining sectors, the same policy instrument could amplify misallocation rather than correct it. In this sense, industrial policy is not inherently good or bad—it is conditional on targeting.

Third, the results highlight an important trade-off between allocation and selection. While credit support can improve the distribution of resources across sectors, it may also weaken the exit of low-productivity firms. This suggests that policy design should not rely on a single instrument. Complementary measures, such as improving firm exit mechanisms or tightening financial discipline, can help mitigate these side effects and enhance overall welfare.

Finally, these findings point to a broader perspective: industrial policy is best understood as part of a policy system. Its effectiveness depends on how it interacts with market structure, financial frictions, and other institutional features of the economy.

Conclusion

The debate over industrial policy is often framed in simple terms—intervention versus laissez-faire. This paper suggests a more nuanced view. In an economy where resources are already misallocated, well-targeted policies can improve efficiency by redirecting capital toward higher-return activities, even if they introduce distortions at the firm level. The key question is therefore not whether governments should intervene, but whether their interventions align with underlying economic distortions. In this sense, industrial policy, when properly targeted, is not just a distortion—it is a correction.

References

Barwick, P. J., H. Kwon and S. Li (2024), “Attribute-based Subsidies and Market Power: an Application to Electric Vehicles,” working paper.

Barwick, P. J., Kalouptsidi, M., and Zahur, N. (2025), “Industrial Policy Implementation: Empirical Evidence from China’s Shipbuilding Industry,” Review of Economic Studies, 92 (6), 3611-3648.

Chang, C., K. Chen, D. Waggoner and T. Zha (2016), “Trends and Cycles in China's Macroeconomy,” NBER Macroeconomics Annual, Vol. 30 (lead article), 1-84.

Chang, J. and W. Xiong. (2026), “Monetary Policy in Mandarin Capitalism,” working paper.

Chen, Kaiji and Tao Zha (2025), “China’s Macroeconomic Development: The Role of Gradualist Reforms,” Journal of Economic Literature, 63(4), 1131-1162.

Chen, K., Y. Huang, X. Liu., Z. Lu, and Y. Wang (2026), “Preferential Credit Policy with Sectoral Markup Heterogeneity,” Journal of International Economics, 161, 104238.

Fang, H., M. Li and G. Lu (2025), “Decoding China’s Industrial Policies”, working paper.

Song, Z., K. Storesletten, and F. Zilibotti. (2011), “Growing Like China,” American Economic Review, 101(1), 196–233.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017