A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email When Forward-Looking Accounting Meets an Unexpected Crisis: Does the Expected Credit Loss Model Amplify Economic Downturns?

This article examines whether the expected credit loss (ECL) model, introduced to make bank provisioning more forward-looking, can inadvertently amplify downturns when a crisis arrives without warning. Using China’s staggered ECL adoption and granular loan-level data from the COVID-19 period, we show that ECL banks cut lending more sharply, raised spreads, and became more selective than incurred credit loss banks serving the same borrowers, with persistent consequences for firms. The evidence highlights a policy tradeoff: forward-looking provisioning improves screening and loan quality, but may need countercyclical safeguards to avoid tightening credit precisely when firms need it most.

The accounting reform that was supposed to fix procyclicality

The 2008 global financial crisis exposed a fundamental flaw in how banks recognized loan losses. Under the traditional incurred credit loss (ICL) approach, banks could only set aside provisions after losses had materialized, a practice widely criticized as “too little, too late” (Bischof et al. 2021). In response, the International Accounting Standards Board and the Financial Accounting Standards Board introduced a new framework: the expected credit loss (ECL) model, which requires banks to recognize provisions based on forward-looking estimates of future losses. The logic was intuitive — by building buffers early in the credit cycle, banks would be better prepared when downturns arrived, thereby reducing procyclicality.

Yet from the outset, academics and policymakers raised a troubling counterpoint. Theoretical work by Abad and Suarez (2018) and Bertomeu et al. (2023) warned that ECL could paradoxically worsen credit crunches at the onset of economic crises. If banks fail to anticipate a downturn — as is inevitable with truly unexpected shocks — the forward-looking model may force a sudden, sharp increase in provisions precisely when lending is most needed. Borio and Restoy (2020) highlighted the COVID-19 pandemic as exactly such a scenario: no model could have predicted it, limiting ECL’s supposed advantage of early buffer-building.

Empirical evidence on this question has been growing. Chen et al. (2025) find that U.S. banks adopting the current expected credit loss (CECL) standard before COVID-19 increased provisions and reduced loan growth during the recession, and Yang (2025) documents a similar credit-supply reduction along with greater loan sales after origination. Granja and Nagel (2025) find that CECL increased consumer loan interest rates, while Kim et al. (2023) show that CECL improved banks’ information production, screening, and monitoring. However, studying ECL’s procyclical effects in the US is complicated by massive government stimulus programs — particularly the Paycheck Protection Program — and the partly voluntary nature of CECL adoption under the CARES Act.

China as a testing ground

In a recent study (Chen and Huang 2026), we use China as a useful and relatively clean empirical setting to investigate whether the ECL model exacerbated the credit crunch during COVID-19. China offers two critical advantages for identification. First, the adoption of ECL was mandatory and staggered: publicly listed banks were required to implement the new standard by 2018 or 2019, while nonlisted banks continued using the ICL approach. This creates a useful treatment-control comparison. Second, unlike the US and Europe, China did not deploy large-scale stimulus packages that channeled liquidity directly to firms through banks, making it easier to isolate the accounting standard’s effects on credit supply.

Using administrative loan-level data from a major Chinese province covering January 2018 to December 2021 — over 540,000 firm-bank-month observations — we employ a difference-in-differences strategy with firm-by-time and firm-by-bank fixed effects. This approach, following Khwaja and Mian (2008), compares lending by ECL and ICL banks to the same firm at the same time, effectively controlling for changes in borrower demand, while also comparing the same firm-bank relationship before and after the pandemic. As a result, differential changes in lending are more likely to reflect supply-side decisions by banks rather than shifts in firms’ credit demand or preexisting borrower-bank matching.

ECL banks pulled back when it mattered most

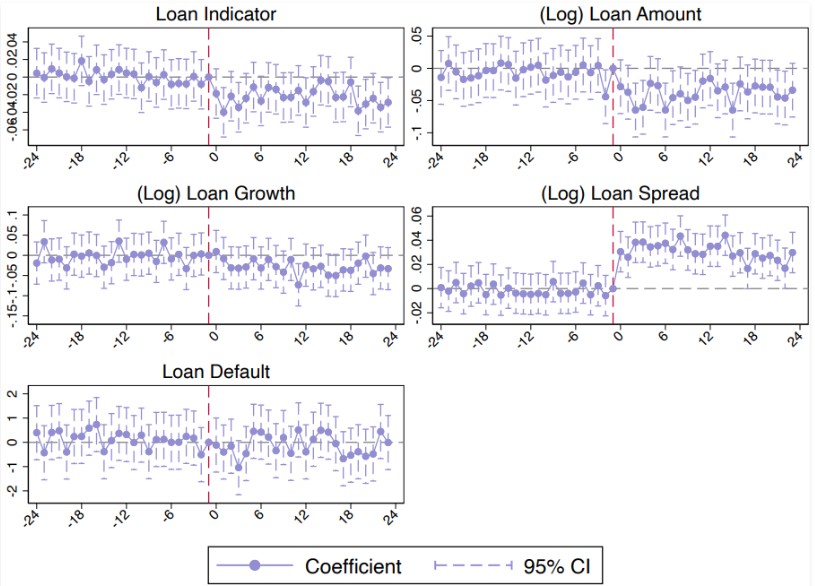

Our results paint a consistent picture. After the COVID-19 outbreak, ECL banks were significantly less likely to originate new loans, and conditional on lending, they provided smaller amounts — a reduction of 1.7% to 3.2% depending on the specification. They also charged higher interest rate spreads (approximately 3.3% higher) and experienced lower default rates on their loan portfolios. In short, ECL banks became markedly more conservative.

Figure 1. Dynamic Effects of the COVID-19 Pandemic on Loan Outcomes

Note: In this figure, we plot the estimation coefficients for the dynamic difference-in-differences regressions that explore the impact of the COVID-19 pandemic on loan-level variables, including the loan indicators, (log) loan amount, (log) loan growth, (log) loan spread, and loan default rate. The dashed vertical lines indicate the month before the outbreak of the pandemic. Standard errors are clustered at the bank-month level. Whiskers denote 95% confidence intervals.

Admittedly, ECL and ICL banks are not identical institutions. Listed ECL banks tend to be larger and more visible to regulators, and are likely to have more sophisticated internal risk-control systems than nonlisted ICL banks. The empirical design therefore does not rely on a simple comparison of average lending across the two groups. Instead, the main tests compare loans by ECL and ICL banks to the same borrower in the same month, while also holding constant persistent firm-bank relationships. This structure absorbs time-varying borrower demand and stable matching patterns, so the remaining difference is a within-borrower, within-period difference in bank supply.

Several additional tests further connect the result to the accounting model rather than to generic bank heterogeneity.The contraction is strongest among ECL banks that recorded larger month-to-month increases in loan loss allowances, and it is driven mainly by provisions on non-defaulted loans — stages 1 and 2 — where ECL’s forward-looking measurement differs most clearly from ICL. The results also survive propensity score matching and entropy balancing on borrower characteristics, and they are sharper for high-risk borrowers, consistent with ECL-induced screening rather than a broad retreat by all large or more regulated banks. These tests cannot eliminate every possible difference between listed and nonlisted banks, but they substantially narrow the interpretation toward the ECL channel (Mahieux et al. 2023).

Real consequences for the corporate sector

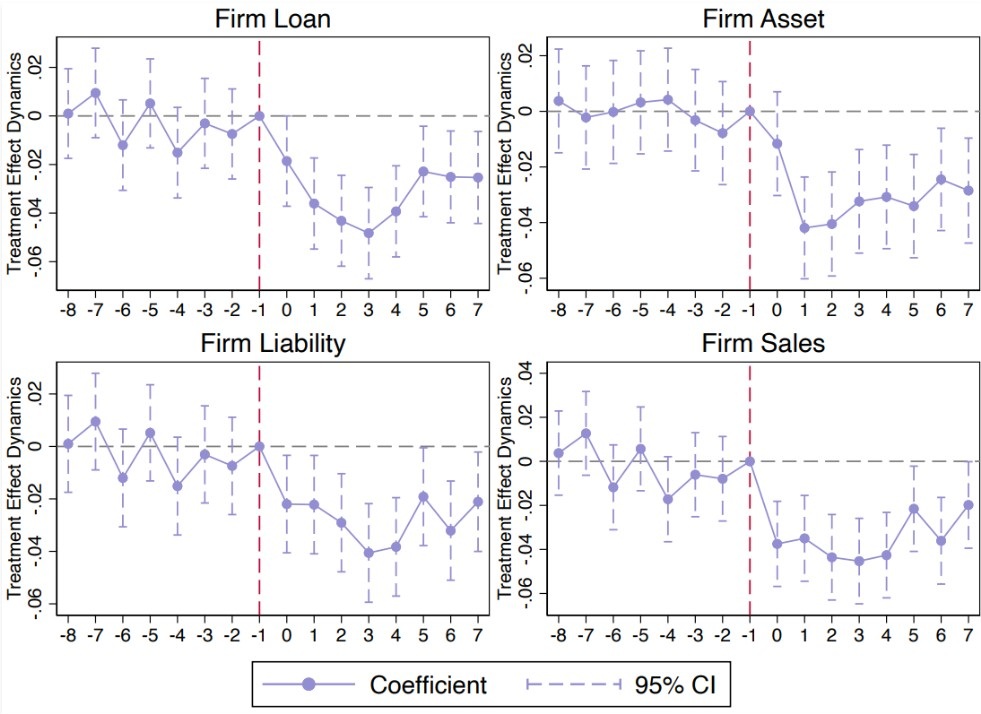

The credit contraction was not merely a banking-sector phenomenon. Firms with greater pre-pandemic dependence on ECL banks — measured by the share of their total borrowing from such banks — experienced significantly worse outcomes. A one standard deviation increase in ECL exposure was associated with a 3.0% decline in total bank loans, a 3.0% reduction in assets, a 2.5% decrease in liabilities, and a 3.3% drop in operating revenue. These effects were amplified for firms that received larger credit cuts and for higher-risk borrowers.

Figure 2. Dynamic Effects of the COVID-19 Pandemic on Firm Real Effects

Note: In this figure, we plot the estimation coefficients for the dynamic difference-in-differences regressions that explore the impact of the COVID-19 pandemic on firm-level variables, including the effects on (log) firm loans, (log) firm assets, (log) firm liabilities, and (log) firm sales. The dashed vertical lines indicate the month before the outbreak of the pandemic. Standard errors are clustered at the firm-quarter level. Whiskers denote 95% confidence intervals.

Crucially, the effects persisted. Our dynamic analysis shows that the divergence in lending between ECL and ICL banks emerged immediately after the outbreak and remained significant throughout our two-year post-pandemic sample period — well after the acute phase of COVID-19 had subsided in China. The real effects on firms similarly persisted across all eight post-pandemic quarters we observe.

A back-of-the-envelope calculation underscores the aggregate stakes: If China’s 59 listed ECL banks had instead used ICL for loan decisions during this period, an estimated additional 4.37 trillion RMB in loans could have been originated — a figure that is meaningful relative to China’s total aggregate financing of 314.13 trillion RMB at year-end 2021.

Policy implications

Our findings speak directly to an ongoing global debate. The ECL model was designed to solve a real problem: the delayed recognition of losses that amplified the 2008 crisis. But our evidence suggests that the cure may introduce its own disease: when crises arrive without warning, as pandemics do, the forward-looking model can trigger a sharp, procyclical credit contraction precisely at the worst moment.

This does not necessarily mean ECL should be abandoned. The lower default rates we document suggest that ECL banks made better lending decisions in some respects. The challenge for policymakers is how to preserve these benefits while mitigating the procyclical amplification. Potential solutions include countercyclical regulatory buffers that explicitly account for ECL dynamics, or temporary relief measures — similar to those some jurisdictions adopted during COVID-19 — that prevent mechanistic provisioning from spiraling into credit crunches.

What our study makes clear is that accounting standards are not merely technical bookkeeping rules. They shape bank behavior, credit allocation, and ultimately the real economy — particularly during the crises when getting these decisions right matters most.

Chen Chen, Monash University, and Difang Huang, Chinese Academy of Sciences

References

Abad, Jorge, and Javier Suarez. 2018. “The Procyclicality of Expected Credit Loss Provisions.” CEPR Discussion Paper No. 13135. https://cepr.org/publications/dp13135.

Bertomeu, Jeremy, Lucas Mahieux, and Haresh Sapra. 2023. “Interplay Between Accounting and Prudential Regulation.” Accounting Review 98 (1): 29–53. https://doi.org/10.2308/TAR-2018-0705.

Bischof, Jannis, Christian Laux, and Christian Leuz. 2021. “Accounting for Financial Stability: Bank Disclosure and Loss Recognition in the Financial Crisis.” Journal of Financial Economics 141 (3): 1188–1217. https://doi.org/10.1016/j.jfineco.2021.05.016.

Borio, Claudio, and Fernando Restoy. 2020. “Reflections on Regulatory Responses to the Covid-19 Pandemic.” FSI Briefs No. 1. https://www.bis.org/fsi/fsibriefs1.pdf.

Chen, Chen, and Difang Huang. 2026. “A Tale of Two Banks: When Credit Loss Models Meet Economic Crises.” Journal of Accounting Research. https://doi.org/10.1111/1475-679X.70030.

Chen, Jing, Yiwei Dou, Stephen G. Ryan, and Youli Zou. 2025. “The Effect of the Current Expected Credit Loss Approach on Banks’ Lending During Stress Periods: Evidence from the COVID-19 Recession.” Accounting Review 100 (1): 113–38. https://doi.org/10.2308/TAR-2022-0275.

Granja, João, and Fabian Nagel. 2025. “Current Expected Credit Losses and Consumer Loans.” Journal of Accounting and Economics 80 (1): 101781. https://doi.org/10.1016/j.jacceco.2025.101781.

Khwaja, Asim Ijaz, and Atif Mian. 2008. “Tracing the Impact of Bank Liquidity Shocks.” American Economic Review 98 (4): 1413–42. https://doi.org/10.1257/aer.98.4.1413.

Kim, Sehwa, Seil Kim, Anya V. Kleymenova, and Rongchen Li. 2023. “Current Expected Credit Losses (CECL) Standard and Banks’ Information Production.” SSRN Electronic Journal. https://dx.doi.org/10.2139/ssrn.4117869.

Mahieux, Lucas, Haresh Sapra, and Gaoqing Zhang. 2023. “CECL: Timely Loan Loss Provisioning and Bank Regulation.” Journal of Accounting Research 61 (1): 3–46. https://doi.org/10.1111/1475-679X.12463.

Yang, Hsiang-Chieh A. 2025. “How Does Loan Loss Accounting Influence Bank Lending? Evidence from the Current Expected Credit Loss (CECL) Model.” Accounting Review 100 (2): 465–90. https://doi.org/10.2308/TAR-2022-0511.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017