A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Fintech Lending and Cashless Payments

Banks have long dominated lending thanks to their informational advantages over borrowers, but fintech lenders are leveling the playing field by exploiting an unexpected data source: cashless payments. Using loan application data from a leading Indian FinTech lender, we show that small businesses that rely more on digital payments are significantly more likely to obtain a loan and receive lower interest rates, and are less likely to default—even after controlling for conventional credit scores. The mechanism is akin to “digital collateral”: cashless payment records are costly for bad borrowers to share, because they expose cash-diverting behaviors, while simultaneously making good borrowers' other signals more credible. These findings carry direct relevance for China, where platforms such as Alipay and WeChat Pay have built precisely this kind of informational synergy between digital payments and lending at scale—and where ongoing debates about big tech regulation and data privacy make the core trade-off between lending efficiency and borrower privacy especially timely.

Banks have traditionally dominated lending, benefiting from both informational advantages and a data monopoly that have been difficult for competitors to overcome (Diamond 1991, Rajan 1992). Despite these barriers, the past decade has seen a dramatic rise in lending by financial technology (fintech) companies. At the same time, payment services have undergone rapid digitalization and disintermediation away from banks, particularly for small-value payments. Compared to cash payments, cashless payments generate significantly more precise information about borrowers’ income and expenses. This information is produced at low cost and can be easily used by tech-savvy lenders operating outside traditional banking relationships, especially in the context of open banking (Parlour et al. 2022, He et al. 2023).

Bridging these two trends, our paper provides a novel answer to the important question of how fintech lending levels the playing field with banks, and even dominates certain lending markets (Berg et al. 2022). We document the existence of an informational synergy between cashless payments and fintech lending and discuss its implications for the future of banking. Borrowers’ use of payment technologies with varying levels of informational precision appears to significantly influence their access to capital from fintech lenders.

To conduct our empirical analysis, we use comprehensive loan application-level data from a leading fintech lender in India (Indifi), which focuses on unsecured lending to small businesses. We first develop a text-analysis methodology to classify each transaction from the payment records into cash and cashless payments. Within cashless payments, we can further separate between information-intensive and information-light methods of payments, depending on whether payments are partly aggregated and whether the payment counterparty is identifiable. We next construct measures of the use of cashless payments at the application level by calculating the value-weighted share of transactions executed with cashless payments, either aggregating or separating inflows and outflows.

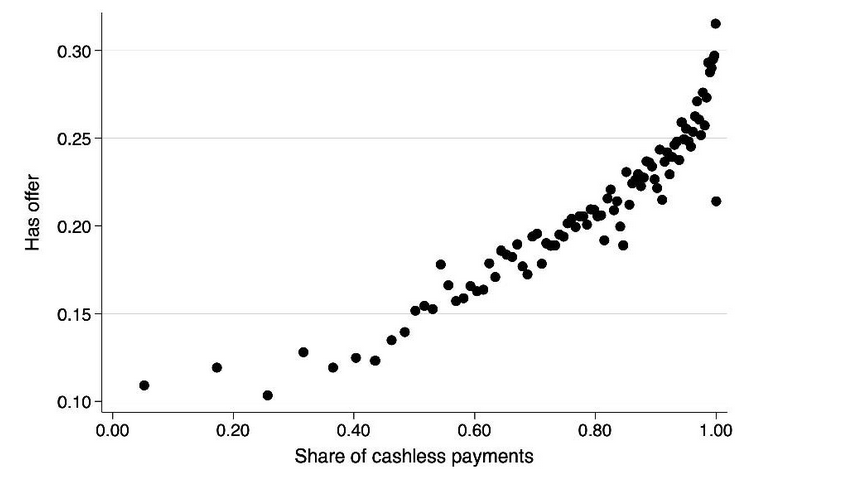

Cashless payments as a predictor of better credit access

We find that a higher use of cashless payments is associated with improved access to capital from fintech lenders. Equipped with our comprehensive data and the measures of payment technology usage, we study how cashless payment usage of varying types and informational precision predicts financing outcomes from fintech lending along both the extensive and intensive margins. We control nonlinearly for a comprehensive set of firm characteristics such as size, age, three-digit zip code, and business owner's credit score.

Although the information revealed by cashless payments can be positive or negative, we find that applicants with a higher share of cashless payments on their record are on average significantly more likely to obtain a loan, and they receive lower interest rates and a higher loan amount conditional on their loans being approved. These results are robust to a host of alternative specifications and measures of cashless payment use, which suggests that the findings are unlikely to be driven by measurement errors or unobserved variable bias.

Moreover, we find a large economic magnitude for these relationships. Controlling for other observable characteristics, including business owner credit score and applicant industry, a one-standard-deviation increase in cashless payment use is associated with an increase in the likelihood of obtaining a loan by 2 percentage points, or 10% of the baseline. Conditional on obtaining a loan, a one-standard-deviation increase in cashless payment use corresponds to a decrease in interest rate of 50 basis points (bps), and an increase in approved loan amount of 14%.

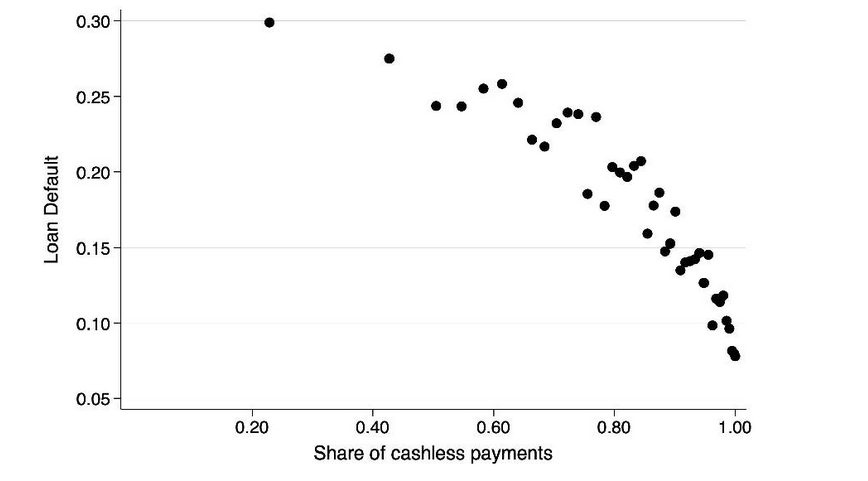

Cashless payment usage as a predictor of lower default

We also find that successful applicants who use more cashless payments are significantly less likely to default, all else being equal. A one-standard-deviation increase in cashless payment use corresponds to a 2 percentage point reduction in default probability, or a 13% reduction from the baseline probability. This result is robust to controlling for the general set of borrower characteristics, including business owner’s credit score, as well as for the intensive-margin outcomes of loan screening such as interest rate and loan amount. This finding provides a direct rationale for fintech lenders to screen based on cashless payment usage, and strengthens the external validity of the previous findings.

The empirical results above raise an important question: why does borrowers’ use of cashless payments in itself (rather than the content) matter for lending decisions and financing outcomes, and with such large economic significance? While it is natural to expect that obvious directional signals derived from payment records (e.g., observing fines or gambling expenses) should be predictive of creditworthiness, payment technology usage itself is a priori neutral in that regard. The pronounced relationship between cashless payment use and default strongly suggests that payment technology choice correlates with borrower creditworthiness. This finding is broadly consistent with Berg et al. (2020), who found that customers’ “digital footprints” complement rather than substitute for credit bureau information in predicting default outcomes. To further flesh out the economic mechanism, we conduct several additional tests uniquely enabled by our data to highlight two complementary economic effects. We then develop a simple model to articulate and unify these effects formally.

Digging in the mechanism(s) at play

We first highlight the findings regarding cashless payments and defaults as a selection effect: less creditworthy applicants are less likely to use cashless payments because the resulting payment records may reveal their lower credit quality, or provide a benchmark that will facilitate the identification of bad behaviors detrimental to the lender. Building further on this rationale, we show that the share of cashless payments in outflows has stronger predictive power for financing outcomes and default compared to that in inflows in terms of both statistical significance and economic magnitude. This finding is consistent with the hypothesis that high usage of cashless payments and the transparency it brings reduces the possibility of conducting cash-flow-diverting activities, such as using company resources for personal spending, and in turn the likelihood of default. Moreover, we show that the predictive power of the cashless payment share on financing outcomes is more pronounced for information-intensive payment records, that is, those with verifiable counterparty information, as opposed to information-light payment records, such as aggregated or anonymized payments. We view these results as consistent with a disciplining effect of informative payment records, which in turn might facilitate borrower sorting into technologies.

We further find that the positive effects of using cashless payments on financing outcomes are significantly stronger for firms exhibiting other signals of high creditworthiness. We use two distinct signals: the applicant’s credit score, which is easily accessible by any lender, and the volatility of payment outflows, which can be uniquely constructed from the content of payment records and proxies for risk. We highlight this complementarity as an accuracy effect in that high cashless payment usage makes other signals more informative, which allows good borrowers to earn even more favorable financing outcomes.

To unify our empirical findings and formalize the selection and accuracy effects, we finally develop a theoretical model that builds on Parlour et al. (2022). The model provides further insights about why lenders incorporate borrowers’ use of cashless payments in their screening decision. The key intuition is that cashless payment records provide a benchmark for production outcomes. This benchmark matters particularly in case of default, when the discovery of potential resource-diverting activities may lead to future legal or economic penalties to the borrower. Cashless payment records thus serve as a form of “digital collateral” because it is more costly for bad borrowers to “post” their records. Our model also connects to the idea of instrumental privacy preferences as studied in Chen et al. (2025), in that bad borrowers face a higher cost in sharing their payment records.

Policy implications

Broadly, our findings provide an economic rationale for the joint rise of fintech lending and cashless payments, as well as for the emergence of fintech platforms and big tech lending. As standalone payment firms and online marketplaces increasingly offer loan products, they are able to capitalize on the informational synergy between cashless payment processing and lending. Globally, Amazon and Alibaba are notable examples of marketplaces that now offer loans to their partners, a trend known as “big tech lending” (Liu et al. 2022). Furthermore, our study provides a strong economic justification for expanding access to historical payment records, as seen with open banking regulatory initiatives.

Our findings carry particular relevance for China, which has experienced perhaps the world’s most dramatic adoption of cashless payments and big tech lending. Platforms such as Alipay and WeChat Pay have built vast ecosystems that integrate digital payments with credit provision, exemplifying the informational synergy we document. Ant Group’s lending operations, for instance, have leveraged the rich transaction data generated by Alipay users to extend credit to hundreds of millions of small businesses and consumers who were previously underserved by traditional banks. Our framework suggests that this integration is not merely a matter of convenience but reflects a deeper economic logic: the payment data generated within these ecosystems serves as “digital collateral” that enables more efficient screening. At the same time, China’s evolving regulatory landscape around data privacy and platform lending, including recent reforms to rein in big tech credit and strengthen data protection, highlights the tension between the informational benefits of cashless payment data and the privacy concerns our model identifies. As China continues to refine its regulatory framework for fintech, the selection and accuracy effects we uncover offer useful guidance for balancing the promotion of financial inclusion with the protection of borrower privacy.

References

Berg, Tobias, Valentin Burg, Ana Gombović, and Manju Puri. 2020. “On the Rise of FinTechs: Credit Scoring Using Digital Footprints.” Review of Financial Studies 33 (7): 2845–97. https://doi.org/10.1093/rfs/hhz099.

Berg, Tobias, Andreas Fuster, and Manju Puri. 2022. “FinTech Lending.” Annual Review of Financial Economics 14: 187–207. https://doi.org/10.1146/annurev-financial-101521-112042.

Chen, Long, Yadong Huang, Shumiao Ouyang, and Wei Xiong. 2025. “Data Privacy and Digital Demand.” Princeton University Working Paper. https://wxiong.mycpanel.princeton.edu/papers/Privacy_Paradox.pdf.

Diamond, Douglas W. 1991. “Monitoring and Reputation: The Choice between Bank Loans and Directly Placed Debt.” Journal of Political Economy 99 (4): 698–721. https://www.jstor.org/stable/2937777.

Ghosh, Pulak, Boris Vallee, and Yao Zeng. 2026. “FinTech Lending and Cashless Payments.” Journal of Finance 81 (2): 1053–1101. https://doi.org/10.1111/jofi.70003.

He, Zhiguo, Jing Huang, and Jidong Zhou. 2023. “Open Banking: Credit Market Competition When Borrowers Own the Data.” Journal of Financial Economics 147 (2): 449–74. https://doi.org/10.1016/j.jfineco.2022.12.003.

Liu, Lei, Guangli Lu, and Wei Xiong. 2024. “The Big Tech Lending Model.” Princeton University Working Paper. https://wxiong.mycpanel.princeton.edu/papers/BigTech.pdf.

Parlour, Christine A., Uday Rajan, and Haoxiang Zhu. 2022. “When FinTech Competes for Payment Flows.” Review of Financial Studies 35 (11): 4985–5024. https://doi.org/10.1093/rfs/hhac022.

Rajan, Raghuram G. 1992. “Insiders and Outsiders: The Choice between Informed and Arm’s-Length Debt.” Journal of Finance 47 (4): 1367–1400. https://doi.org/10.1111/j.1540-6261.1992.tb04662.x.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017