A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Equity Financing and Exports: Evidence from IPO Approvals in China

Access to public equity through IPOs enables Chinese exporters to expand into more foreign markets by financing the intangible investments and risk taking that bank credit alone cannot support, suggesting that well-functioning equity markets are a critical but overlooked ingredient for export-led growth in developing countries.

When policymakers in developing countries seek to promote exports, they typically reach for familiar tools: trade facilitation, export subsidies, or expanded bank lending. A large body of research supports this instinct. Financial development shapes countries’ comparative advantage in international trade (Manova 2013), and firm-level studies confirm that access to bank credit and trade finance matters for export performance (Paravisini et al. 2015, Antràs and Foley 2015).

However, nearly all the evidence concerns debt financing. Whether equity markets matter for exports, and if so how, has received almost no empirical attention. Corporate finance theory tells us that equity and debt serve fundamentally different purposes. Debt is well suited to funding tangible assets with predictable cash flows. Equity, by contrast, can finance investments whose payoffs are uncertain and hard to collateralize, such as R&D, brand building, and market exploration (Brown et al. 2009). For firms trying to break into new foreign markets, where success often hinges on exactly these kinds of intangible, risky investments, the distinction could be consequential.

A natural experiment in China’s IPO system

In Gong et al. (2025), we provide the first micro-level evidence on how access to public equity through initial public offerings affects firm exports. We exploit a distinctive feature of China’s capital markets: the approval-based IPO system that was in place until 2023. Unlike the registration-based systems in the United States and Europe, China’s system required firms to navigate a multiyear review process overseen by the China Securities Regulatory Commission. Applicants had to meet stringent financial thresholds, undergo multiple rounds of prescreening, and face a final review where a seven-member committee voted on their application. The entire process averaged three years. Even among firms that made it to the final stage, roughly 15% were rejected.

This institutional setting provides a valuable opportunity for causal identification. Firms reaching the final review meeting had already demonstrated strong financial performance and endured years of regulatory scrutiny. Comparing approved and rejected applicants at this stage is analogous to the “million-dollar plants” approach of Greenstone et al. (2010), which identifies causal effects by comparing winning and runner-up locations for large factory investments. To further sharpen identification, we use detailed review meeting records to exclude firms rejected over concerns about future revenue or profitability, since such concerns might reflect fundamental weaknesses that would simultaneously affect export performance.

Combining IPO application records with Chinese customs transaction data from 2000 to 2016, we track the export activities of over 900 manufacturing firms before and after their review meetings.

IPOs expand markets, not just sales

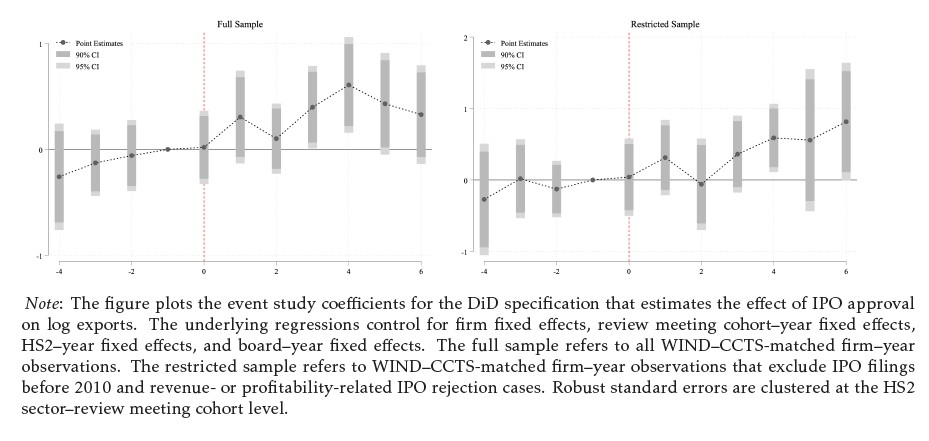

Our difference-in-differences analysis reveals that IPO approval increases firm exports by more than 6% annually over the subsequent six years, a cumulative gain of roughly 37%. Crucially, approved and rejected applicants follow nearly identical export trajectories before their review meetings, with divergence emerging only afterward.

Figure 1

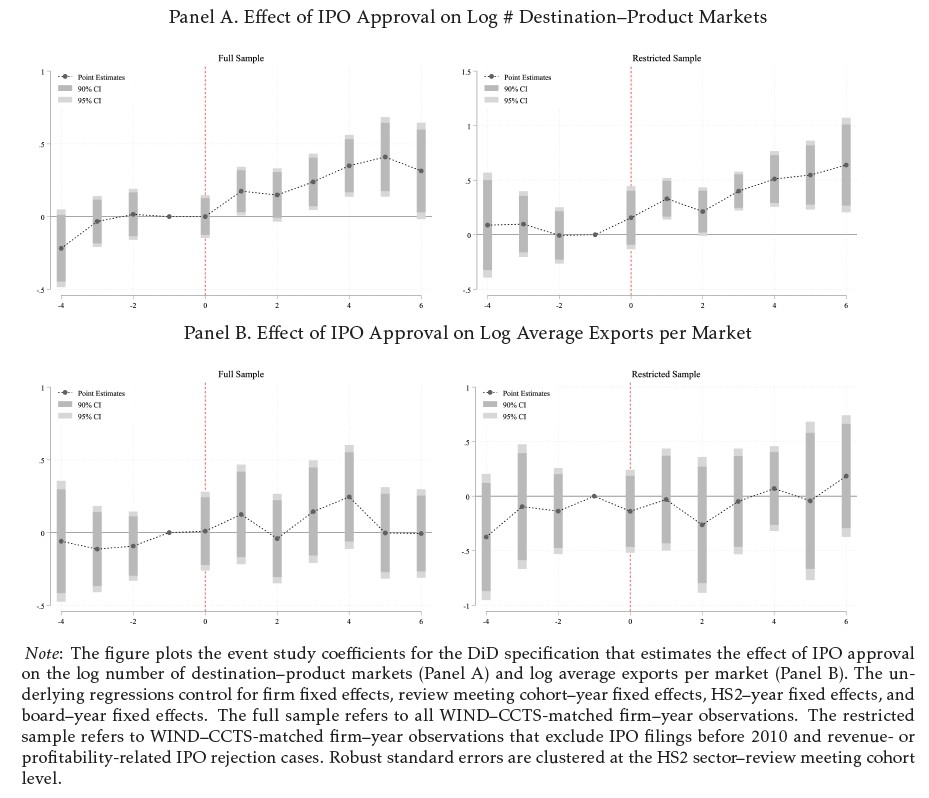

Where does this export growth come from? The answer turns out to be revealing. IPO approval primarily drives expansion along the extensive margin: approved firms enter and stay in more destination–product markets. By contrast, average sales per existing market show little response. In other words, IPO approval helps firms go to new places with new products, rather than simply selling more in markets they already serve.

Where does this export growth come from? The answer turns out to be revealing. IPO approval primarily drives expansion along the extensive margin: approved firms enter and stay in more destination–product markets. By contrast, average sales per existing market show little response. In other words, IPO approval helps firms go to new places with new products, rather than simply selling more in markets they already serve.

Figure 2

This pattern is strikingly different from what we know about bank credit. Paravisini et al. (2015) find that credit supply shocks in Peru primarily affected the intensive margin of exports, with little impact on market entry. The contrast suggests that equity and debt play qualitatively different roles in financing international trade.

Not a substitute for bank loans

Why does equity financing work through such a different channel? One natural hypothesis is that IPOs simply provide an alternative source of capital. If that were the case, we would expect the strongest effects among firms that were most credit constrained before going public. We find the opposite. The export-promoting effect of IPO approval is concentrated among firms with low pre-existing leverage and ample liquidity, the firms that were least constrained in the debt market.

The evidence instead supports the view that equity capital finances activities that debt cannot. Firms with preexisting patent filings or high-selling expense intensity, both indicators of intangible investment capacity, experience significantly larger export gains following IPO approval. Approved firms also disproportionately expand into markets for products with high R&D intensity, high advertising intensity, and greater complexity. These are markets where success depends on innovation, branding, and customization rather than on purely scaling up production.

We also find that IPO approval encourages risk taking in international expansion. Approved firms enter more volatile markets and pioneer into markets where Chinese exporters previously had low penetration. Complementary evidence from balance sheet data shows that IPO approval leads to significant increases in selling expenses and patent filings, while physical capital expenditure responds only modestly. In short, equity capital from IPOs funds the intangible investments and exploratory strategies that banks are unwilling or unable to finance.

What lessons can we draw?

These findings carry direct implications for policymakers, particularly in emerging economies where equity markets remain underdeveloped relative to banking systems. China’s experience illustrates that a well-functioning public equity market can serve as more than a mechanism for raising capital. It can enable leading exporters to undertake the risky, intangible investments required to compete in sophisticated global markets.

The transition from China's approval-based IPO system to a registration-based system, completed in 2023, was motivated partly by concerns that the old system created bottlenecks and allocated listing opportunities inefficiently. Our findings add a trade dimension to this debate: by restricting IPO access, the approval system may have constrained the international expansion of otherwise qualified firms.

Of course, the Chinese context has its own particularities. Private firms in China during our sample period had limited access to alternative forms of equity financing, such as venture capital, which was still underdeveloped. The marginal value of an IPO may therefore be larger in China than in economies with deeper private equity markets. Still, for countries like India, Indonesia, and South Korea, which have maintained or recently reformed their own approval-based IPO systems, the core lesson is clear: policies aimed at promoting exports should look beyond trade facilitation and bank lending. Developing accessible equity markets may be just as important, especially for economies seeking to move into more complex, technology-intensive stages of global value chains.

References

Antràs, Pol, and C. Fritz Foley. 2015. “Poultry in Motion: A Study of International Trade Finance Practices.” Journal of Political Economy 123 (4): 809–852. https://doi.org/10.1086/681592.

Brown, James R., Steven M. Fazzari, and Bruce C. Petersen. 2009. “Financing Innovation and Growth: Cash Flow, External Equity, and the 1990s R&D Boom.” Journal of Finance 64 (1): 151–85. https://doi.org/10.1111/j.1540-6261.2008.01431.x.

Gong, Robin Kaiji, Yao Amber Li, Stephen Teng Sun, and Shang-Jin Wei. 2025. “Equity Financing and Exports: Evidence from IPO Approvals in China.” Journal of International Economics. Forthcoming.

Greenstone, Michael, Richard Hornbeck, and Enrico Moretti. 2010. “Identifying Agglomeration Spillovers: Evidence from Winners and Losers of Large Plant Openings.” Journal of Political Economy 118 (3): 536–98. https://doi.org/10.1086/653714.

Manova, Kalina. 2013. “Credit Constraints, Heterogeneous Firms, and International Trade.” Review of Economic Studies 80 (2): 711–44. https://doi.org/10.1093/restud/rds036.

Paravisini, Daniel, Veronica Rappoport, Philipp Schnabl, and Daniel Wolfenzon. 2015. “Dissecting the Effect of Credit Supply on Trade: Evidence from Matched Credit-Export Data.” Review of Economic Studies 82 (1): 333–59. https://doi.org/10.1093/restud/rdu028.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017