A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Unequal School Enrollment Rights and Increased Inequality: The Case of Shanghai

In Shanghai, housing entitlements with enrollment access to a good public primary school is associated with a 0.1-0.35 percentage point lower annual rental yield. This rental yield gap is the opportunity cost of securing such housing, which is within the affordability range of most middle-income families in Shanghai. This implies that, should there be no credit constraint for homeownership, children from middle-income families should have a higher likelihood of accessing better public education. We find, however, that the enrollment rights between homeowners and renters, together with the credit constraint to own a home, actually lowers the chance of children from middle-income families of attending better public schools relative to those children from families with high initial wealth. This resulting reduced intergeneration mobility exacerbates the social inequality in China.

In Chinese cities, enrollment to public primary school is proximity-based, which is similar to the West. However, what sets China apart from most Western countries is that the enrollment rights to public primary school is unequal across different housing tenures. Children from families who rent property are ranked after those families who own property when applying to public primary schools in most Chinese cities. Since the number of applicants attempting to enter popular public primary schools generally exceeds capacity, children from renting families are essentially excluded. Also, due to both a credit constraint and low user cost (i.e., no property tax), middle-income families or those with decent income but low initial wealth have a lower chance of owning high-valued housing than those families with low income but high initial wealth. Thus, tenure-based discrimination of access to public schools, together with a credit constraint but low user cost to own a home, contributes to the proliferation of unequal access to high-quality public education resources among households in Chinese cities (Zhang and Chen, 2017).

The literature has documented how the value of enrollment privileges to access good schools would be capitalized into the price premium of housing in good school districts, a fact widely observed worldwide (Figlio and Lucas, 2004; Nguyen-Hoang and Yinger, 2011). However, in China, renters are deprived this enrollment privilege to a good school even if they rent within a good school district. We should expect to see that rental rates in good school districts should not be different from comparable rental rates in ordinary school districts; however, we do see a difference. As rental yield is the ratio between rent and housing price, housing in good school districts results in a lower rental yield.

The intuitive gap in the rental yield of housing in good school districts provides us with a rare opportunity to estimate the magnitude of the user cost of attending a good school in China. By merging the dwelling-level seller’s list price and rent information collected from leading online brokers in Shanghai, a matched database is constructed. The database is further matched to neighborhood information using GIS data and each neighborhood is paired with its associated school district. The data used in the analysis includes samples of 6,526,102 listings in 700 neighborhoods from 12 of 14 administrative districts in Shanghai between July 2013 and November 2014.

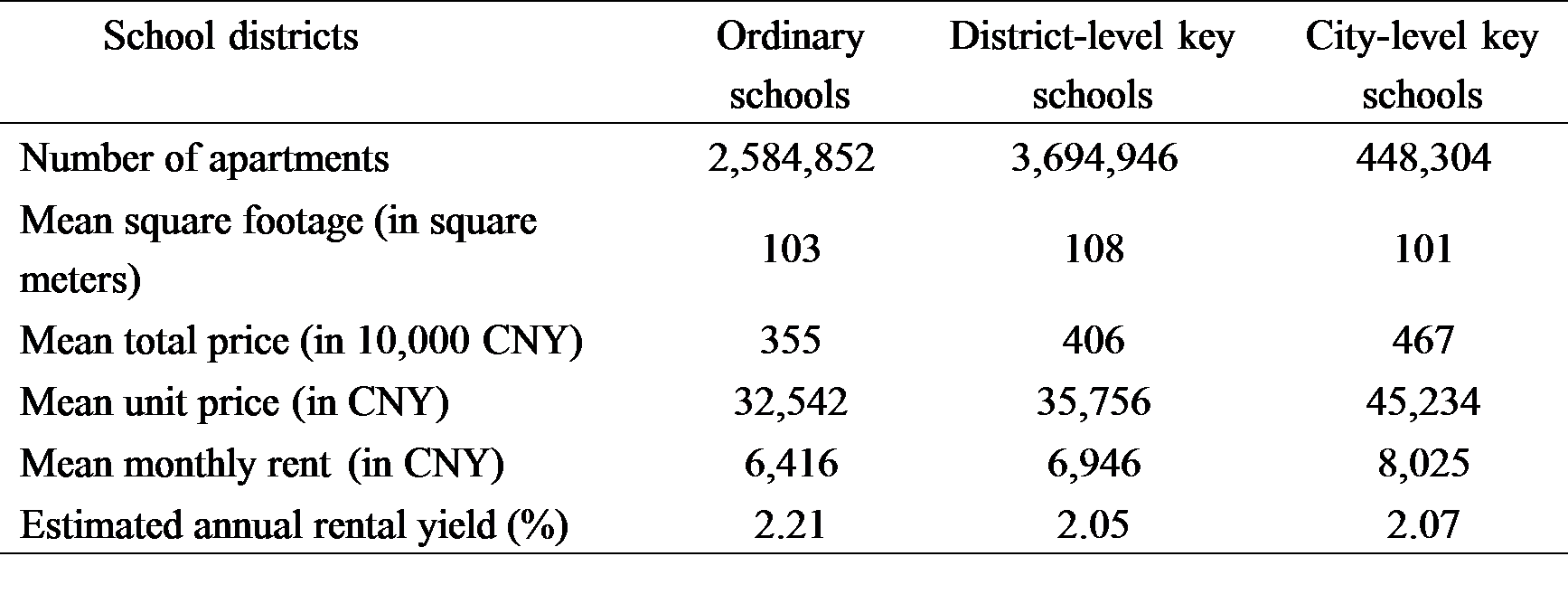

Table 1 shows the comparison of the list price and list rent of apartments associated with ordinary, district-level, and city-level key schools, and the summary statistics of key characteristics of these three types of apartments. All three types of apartments share similar means of square footage, but the prices for both resale and rent are much higher for key schools. However, the rent yield cannot be directly calculated from the data because few apartments are simultaneously listed for resale and for rent. To estimate the annual rental yield, we employ a neighborhood-wide hedonic pricing model for rents. Specifically, we use a hedonic pricing model to predict the market rent of each apartment in the sample in two stages. This is done in the first stage by regressing the logarithm of monthly rent of a certain apartment to the characteristics of the apartment, such as square footage, the number of bedrooms, the floorplan of apartment, and the total floorplan of the building. A neighborhood-specific coefficient is allowed and the monthly effect is included in this regression. In the second stage, applying the first-stage imputed coefficients of the apartment characteristics on resale samples in the same neighborhood, we are able to predict the market rent of all apartments. Thus, we obtain the imputed annual rental yield for each apartment. As shown in Table 1, on average, the imputed annual rental yields for apartments with ordinary, district-level, and city-level key schools are 2.21 percent, 2.05 percent, and 2.07 percent, respectively.

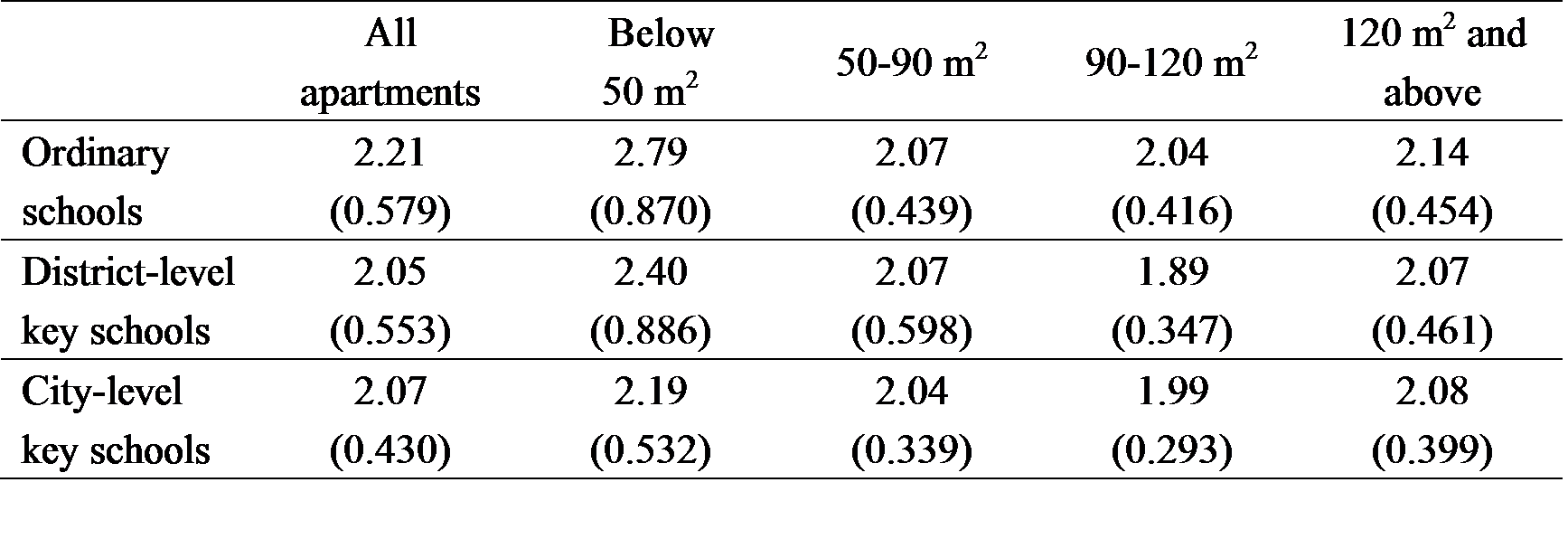

Table 2 reports the imputed annual rental yield grouped by school quality and dwelling size. The results show a clear gap in the annual rental yield of housing across ordinary and key school districts at different levels. The gap is especially large for small-sized apartments less than 50 square meters.

Note: Standard deviations are in parentheses.

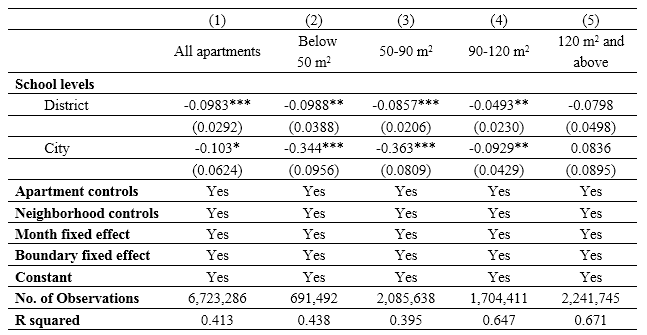

The imputed annual rental yield of each housing unit is then regressed on its neighborhood’s corresponding school quality to estimate the willingness-to-pay (WTP) of residents to access the associated public education resources. A large set of neighborhood-level and dwelling-level apartment characteristics are included in the regression. By controlling the school district-level boundary fixed effect (comparing housing within and outside of the boundary), the locality difference as well as the difference in living conditions that simultaneously affect rent and price across the school district’s boundary is eliminated. We are thereby assured that the estimated difference in rent yields only comes from the difference in the neighborhood’s school quality. The estimated results are listed in Table 3.

Note: Robust Standard errors clustered at the neighborhood level. *** p<0.01, ** p<0.05, and * p<0.1.

Table 3 shows that there is a large rental yield discount of both economic and statistical significance for apartments in good school districts. Small and medium-small apartments (below 50 square meters and between 50 and 90 square meters, respectively) suffer the largest discount in rental yield. The discount is as large as a 0.344 percentage point for small apartments and a 0.363 percentage point for medium-small apartments located in city-level key school districts. Medium-large apartments between 90 and 120 square meters suffer a smaller discount but it is still statistically significant; whereas for large apartments that are 120 square meters and above, the discount is not statistically significant. The reason for this difference lies in the fact that for small apartments, enrollment privileges to good schools account for a large share of its value, while the contribution of such enrollment privileges to home value shrinks for large apartments, which are more suitable for families.

In the sample, the average price per square meter for an apartment in a city-level key school district is 45,234 CNY (the exchange rate is 1 USD=6.12 CNY at the sampling period). For an apartment of 90 square meters, which suffers a discount in annual rental yield of 0.363 percentage points, the owner would lose as much as 14,777 CNY in potential rent each year. Furthermore, in many cases homeowners need to purchase the apartment several years before their children reach school age. Assuming a six-year holding period, the potential rent loss for a 90 square meter apartment in a good school district is about 90,000 CNY on average.

The potential rent loss of holding housing in good school districts can be regarded as the user cost of accessing a good school. Compared to the city’s dispensable income per capita (47,710 CNY in 2014) or the annual tuition of the top private schools (30,000-60,000 CNY per year), this is not a large amount. However, the proximity-based rule of public school enrollment limits the choice of public school enrollment and middle-income families are in disadvantaged positions in the competition for good public education resources compared to those with high initial wealth. The proximity-based enrollment rule helps to prevent corruption in public schools’ enrollment, but with the presence of a credit constraint in owning a home, such a policy has also exacerbated social inequality in terms of reduced intergenerational mobility.

As long as there is a considerable difference in school quality or reputation, this difference would be inevitably capitalized in one form or another (Black, 1999). Currently, fiscal spending is largely equalized in public primary schools in Chinese cities. However, public schools still differ considerably in terms of both quality and reputation. More affirmative policies are needed to further equalize public education resources across locations, but such a policy may take a long time to take effect. One quick solution would be to allow renter families to enjoy the same equal enrollment rights as owner families. Such reform will benefit middle-income families with a decent income but low initial wealth. Alternatively, implementing a property tax that adds the cost of asset holding could also improve the positions of middle-income families in both housing market and education market and therefore mitigate inequality. Lastly, although a more developed housing finance market would alleviate the credit constraints of owning a home, it may also boost housing prices generally; thus its net effect to middle-income families is difficult to predict.

Black, S. E. (1999) “Do Better Schools Matter? Parental Valuation of Elementary Education,” Quarterly Journal of Economics 114(2): 577–599. http://www.jstor.org/stable/2587017

Figlio, D. N., and Lucas, M. E. (2004) “What’s in a Grade? School Report Cards and the Housing Market,” American Economic Review 94(3): 591–604. http://pubs.aeaweb.org/doi/10.1257/0002828041464489

Nguyen-Hoang, P., and Yinger, J. (2011) “The Capitalization of School Quality into House Values: A Review,” Journal of Housing Economics 20(1): 30–48. http://linkinghub.elsevier.com/retrieve/pii/S1051137711000027

In Chinese cities, enrollment to public primary school is proximity-based, which is similar to the West. However, what sets China apart from most Western countries is that the enrollment rights to public primary school is unequal across different housing tenures. Children from families who rent property are ranked after those families who own property when applying to public primary schools in most Chinese cities. Since the number of applicants attempting to enter popular public primary schools generally exceeds capacity, children from renting families are essentially excluded. Also, due to both a credit constraint and low user cost (i.e., no property tax), middle-income families or those with decent income but low initial wealth have a lower chance of owning high-valued housing than those families with low income but high initial wealth. Thus, tenure-based discrimination of access to public schools, together with a credit constraint but low user cost to own a home, contributes to the proliferation of unequal access to high-quality public education resources among households in Chinese cities (Zhang and Chen, 2017).

The literature has documented how the value of enrollment privileges to access good schools would be capitalized into the price premium of housing in good school districts, a fact widely observed worldwide (Figlio and Lucas, 2004; Nguyen-Hoang and Yinger, 2011). However, in China, renters are deprived this enrollment privilege to a good school even if they rent within a good school district. We should expect to see that rental rates in good school districts should not be different from comparable rental rates in ordinary school districts; however, we do see a difference. As rental yield is the ratio between rent and housing price, housing in good school districts results in a lower rental yield.

The intuitive gap in the rental yield of housing in good school districts provides us with a rare opportunity to estimate the magnitude of the user cost of attending a good school in China. By merging the dwelling-level seller’s list price and rent information collected from leading online brokers in Shanghai, a matched database is constructed. The database is further matched to neighborhood information using GIS data and each neighborhood is paired with its associated school district. The data used in the analysis includes samples of 6,526,102 listings in 700 neighborhoods from 12 of 14 administrative districts in Shanghai between July 2013 and November 2014.

Table 1 shows the comparison of the list price and list rent of apartments associated with ordinary, district-level, and city-level key schools, and the summary statistics of key characteristics of these three types of apartments. All three types of apartments share similar means of square footage, but the prices for both resale and rent are much higher for key schools. However, the rent yield cannot be directly calculated from the data because few apartments are simultaneously listed for resale and for rent. To estimate the annual rental yield, we employ a neighborhood-wide hedonic pricing model for rents. Specifically, we use a hedonic pricing model to predict the market rent of each apartment in the sample in two stages. This is done in the first stage by regressing the logarithm of monthly rent of a certain apartment to the characteristics of the apartment, such as square footage, the number of bedrooms, the floorplan of apartment, and the total floorplan of the building. A neighborhood-specific coefficient is allowed and the monthly effect is included in this regression. In the second stage, applying the first-stage imputed coefficients of the apartment characteristics on resale samples in the same neighborhood, we are able to predict the market rent of all apartments. Thus, we obtain the imputed annual rental yield for each apartment. As shown in Table 1, on average, the imputed annual rental yields for apartments with ordinary, district-level, and city-level key schools are 2.21 percent, 2.05 percent, and 2.07 percent, respectively.

Table 1: Summary Statistics of Samples

Table 2: Means of Annual Rental Yield by School Quality and Dwelling Size

The imputed annual rental yield of each housing unit is then regressed on its neighborhood’s corresponding school quality to estimate the willingness-to-pay (WTP) of residents to access the associated public education resources. A large set of neighborhood-level and dwelling-level apartment characteristics are included in the regression. By controlling the school district-level boundary fixed effect (comparing housing within and outside of the boundary), the locality difference as well as the difference in living conditions that simultaneously affect rent and price across the school district’s boundary is eliminated. We are thereby assured that the estimated difference in rent yields only comes from the difference in the neighborhood’s school quality. The estimated results are listed in Table 3.

Table 3: Regression Results of Rent Yield Gaps

Table 3 shows that there is a large rental yield discount of both economic and statistical significance for apartments in good school districts. Small and medium-small apartments (below 50 square meters and between 50 and 90 square meters, respectively) suffer the largest discount in rental yield. The discount is as large as a 0.344 percentage point for small apartments and a 0.363 percentage point for medium-small apartments located in city-level key school districts. Medium-large apartments between 90 and 120 square meters suffer a smaller discount but it is still statistically significant; whereas for large apartments that are 120 square meters and above, the discount is not statistically significant. The reason for this difference lies in the fact that for small apartments, enrollment privileges to good schools account for a large share of its value, while the contribution of such enrollment privileges to home value shrinks for large apartments, which are more suitable for families.

In the sample, the average price per square meter for an apartment in a city-level key school district is 45,234 CNY (the exchange rate is 1 USD=6.12 CNY at the sampling period). For an apartment of 90 square meters, which suffers a discount in annual rental yield of 0.363 percentage points, the owner would lose as much as 14,777 CNY in potential rent each year. Furthermore, in many cases homeowners need to purchase the apartment several years before their children reach school age. Assuming a six-year holding period, the potential rent loss for a 90 square meter apartment in a good school district is about 90,000 CNY on average.

The potential rent loss of holding housing in good school districts can be regarded as the user cost of accessing a good school. Compared to the city’s dispensable income per capita (47,710 CNY in 2014) or the annual tuition of the top private schools (30,000-60,000 CNY per year), this is not a large amount. However, the proximity-based rule of public school enrollment limits the choice of public school enrollment and middle-income families are in disadvantaged positions in the competition for good public education resources compared to those with high initial wealth. The proximity-based enrollment rule helps to prevent corruption in public schools’ enrollment, but with the presence of a credit constraint in owning a home, such a policy has also exacerbated social inequality in terms of reduced intergenerational mobility.

As long as there is a considerable difference in school quality or reputation, this difference would be inevitably capitalized in one form or another (Black, 1999). Currently, fiscal spending is largely equalized in public primary schools in Chinese cities. However, public schools still differ considerably in terms of both quality and reputation. More affirmative policies are needed to further equalize public education resources across locations, but such a policy may take a long time to take effect. One quick solution would be to allow renter families to enjoy the same equal enrollment rights as owner families. Such reform will benefit middle-income families with a decent income but low initial wealth. Alternatively, implementing a property tax that adds the cost of asset holding could also improve the positions of middle-income families in both housing market and education market and therefore mitigate inequality. Lastly, although a more developed housing finance market would alleviate the credit constraints of owning a home, it may also boost housing prices generally; thus its net effect to middle-income families is difficult to predict.

(Muyang Zhang, China Public Finance Institute and School of Public Economics and Administration, Shanghai University of Finance and Economics; Jie Chen, School of Public Economics and Administration, Shanghai University of Finance and Economics.)

Black, S. E. (1999) “Do Better Schools Matter? Parental Valuation of Elementary Education,” Quarterly Journal of Economics 114(2): 577–599. http://www.jstor.org/stable/2587017

Figlio, D. N., and Lucas, M. E. (2004) “What’s in a Grade? School Report Cards and the Housing Market,” American Economic Review 94(3): 591–604. http://pubs.aeaweb.org/doi/10.1257/0002828041464489

Nguyen-Hoang, P., and Yinger, J. (2011) “The Capitalization of School Quality into House Values: A Review,” Journal of Housing Economics 20(1): 30–48. http://linkinghub.elsevier.com/retrieve/pii/S1051137711000027

Zhang, M., and Chen, J. (2017) “Unequal School Enrollment Rights, Rent Yields Gap, and Increased Inequality: The Case of Shanghai,” China Economic Review, forthcoming,http://www.sciencedirect.com/science/article/pii/S1043951X17300603.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017