A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email The Geography of Market Power: Rethinking Consolidation in China’s Steel Industry

China’s steel industry is the world’s largest, but it is also famously fragmented. For years, policymakers have pushed for mergers and acquisitions to consolidate the sector, aiming to boost efficiency and create a handful of national champions. Yet a new study shows that whether consolidation succeeds depends not on size alone, but on where and how it happens. Using detailed data on steel flows across China, we reveal that the geography of supply and demand—and the frictions that separate them—are central to understanding market power and the true gains from industrial policy.

Why location matters (and why it’s often overlooked)

Steel is heavy and costly to transport, so markets are largely regional. A firm that dominates one part of the country may barely register in another. This means that simple national concentration ratios—like the share of the top four firms—can be deeply misleading about where market power actually lies.

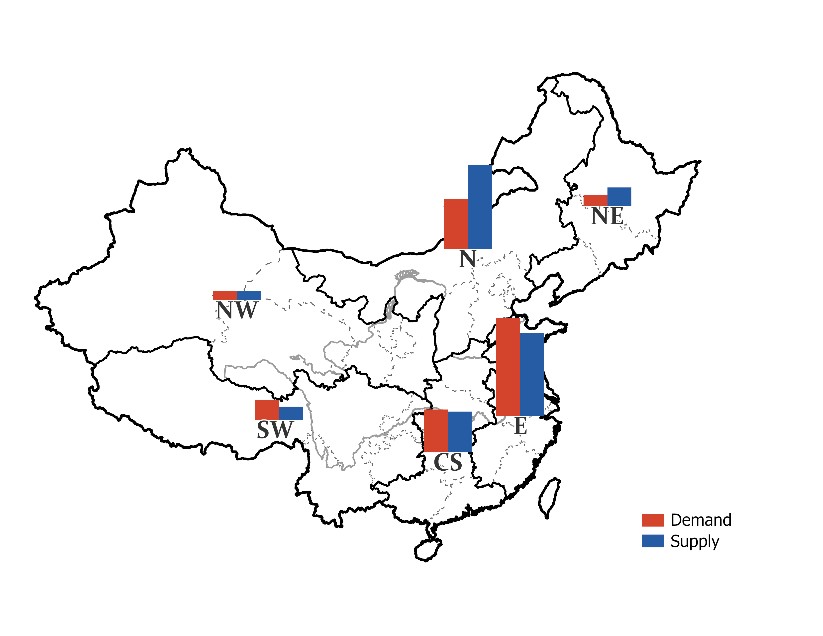

But in China there is a second, equally important geographic reality: production and demand are often far apart. A quarter of all steel output is concentrated in Hebei, a northern province, while a huge share of demand lies in the Yangtze River Delta in the east. This mismatch creates a complex web of cross regional trade. The idea that distance shapes competition is not new—Miller and Osborne (2014) showed similar patterns in the US cement industry—but this paper provides the first such analysis for China’s steel sector, which is an order of magnitude larger and faces distinct institutional frictions.

Figure 1: The geography of steel supply and demand across China’s six regions. Blue bars show production; red bars show consumption. The North produces far more steel than it consumes (a surplus region), while the East—home to the Yangtze River Delta—consumes much more than it produces (a deficit region). This spatial imbalance shapes how consolidation affects local markets and why cross regional flows matter.

The industry also faces three frictions that shape how consolidation plays out:

• Scale bias. Most past mergers and acquisitions (M&A) were directed by the government and involved large firms acquiring smaller rivals, often favoring size over efficiency.

• Local protectionism. Provincial governments tend to prefer “regional” mergers that keep capacity within their borders, rather than cross regional deals that might relocate production.

• Ownership restrictions. Private firms are often limited in their ability to acquire state owned enterprises, narrowing the pool of potential buyers.

How the study works: A model for a spatially complex industry

To move beyond simple concentration ratios and assess how mergers affect the market, we build a model that mirrors the real world decisions of steel buyers and sellers across China.

• On the demand side, the model starts with a simple idea: steel buyers (such as construction firms or car factories) choose where to buy based on three factors: price, product quality, and distance. A buyer in Shanghai may prefer a closer supplier even if it charges slightly more, because shipping steel over long distances is expensive and can disrupt production schedules. The model uses detailed data on regional sales to estimate how sensitive buyers are to price and distance, and to recover the “markups” (the gap between price and cost) that firms enjoy.

• On the supply side, each steel plant has a maximum capacity and produces using a fixed recipe of iron ore, coke, and coal. Some firms are simply more efficient than others—they use less raw material per ton of steel, or they are better managed. We use plant level data on inputs and outputs to measure these differences in productivity and cost. Importantly, we find that private firms are systematically more cost efficient than state owned ones, after accounting for product quality and location. Similar methods have been used to measure productivity and markups in the US steel industry (Collard Wexler and De Loecker 2015), but this paper is the first to embed those productivity differences in a spatial competition framework that captures how distance and regional demand shape market power.

• Competition across regions is modeled as a game in which each firm group sets the prices of the firms it owns, anticipating rivals’ responses. The model accounts for the fact that a firm may be constrained by its production capacity—it cannot sell more steel than its furnaces can produce. Solving this kind of problem with many firms, many regions, and possible capacity constraints is technically challenging, so we develop a new algorithm to find the equilibrium prices and sales.

With this framework in place, we simulate what would happen if ownership changed (through mergers) or if demand shifted (as it did after the real estate slowdown). When firms merge, they no longer set prices independently at each subsidiary. Instead, the merged group chooses a separate price for each subsidiary to maximize total group profit, internalizing competition between its own plants. Post-merger cost reductions enter through two channels: lower iron ore procurement costs (e.g., stronger bargaining power in iron ore markets) and knowledge transfer that allows less productive acquired firms to adopt the cost efficiency of the lead firm. The model provides a disciplined way to separate the effects of market power from genuine efficiency improvements.

The gains from “smarter” mergers

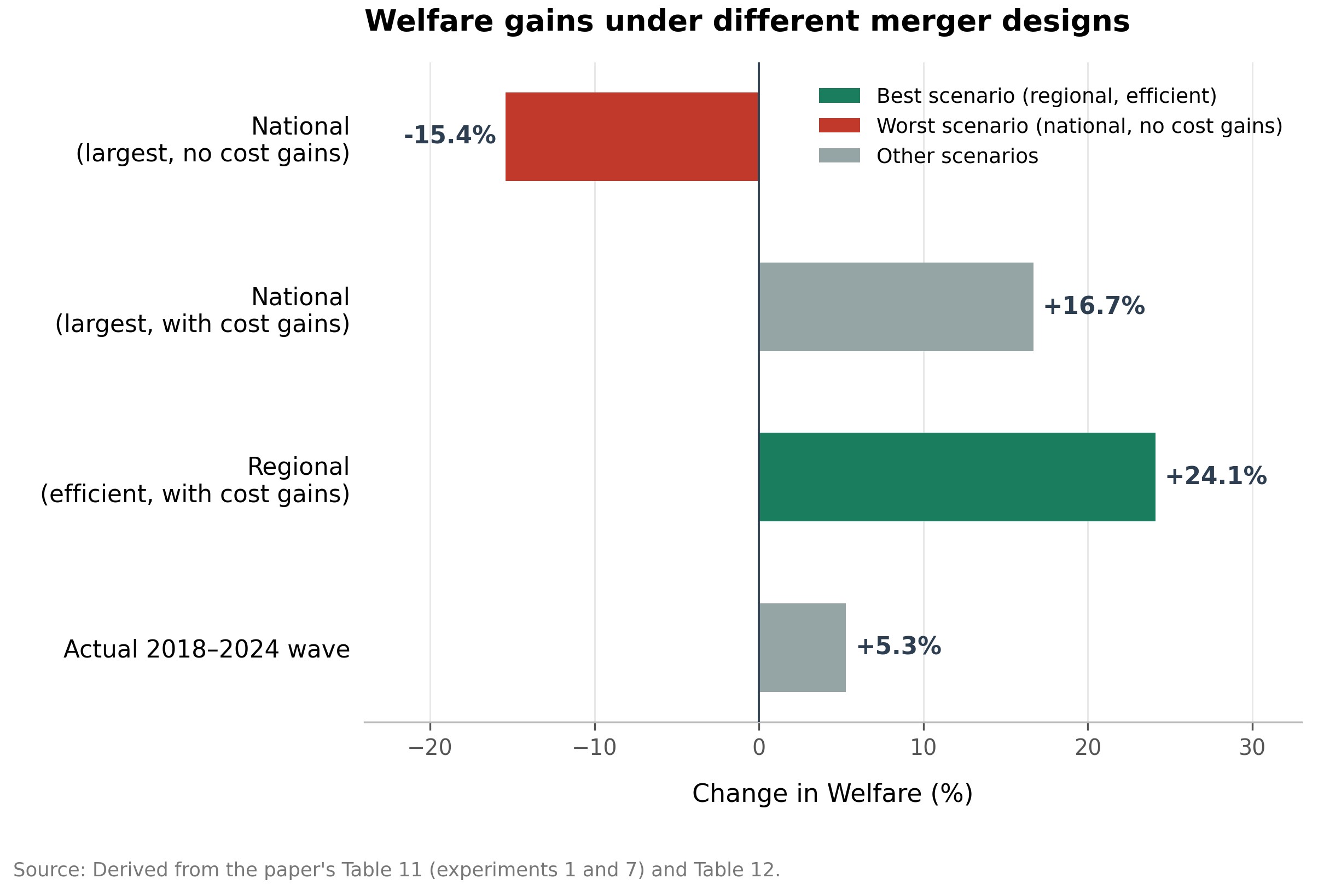

We find that mergers can indeed improve welfare—but only when they are designed well. The best outcomes come from mergers that are regionally focused and led by the most efficient firms. In the most favorable scenario (within region consolidation led by efficient producers), costs fall by 12.5%, prices drop by 4%, and consumer surplus rises by 14%. Total welfare improves by 24%, and market concentration reaches the government’s target of 60–70% of production held by the top ten groups.

Why do regional mergers work so well? Because they allow smaller but more productive firms to lead the consolidation, limiting the expansion of large, less efficient incumbents. They also keep market power contained within geographic markets, preventing a national champion from pushing up prices everywhere. In contrast, mergers driven by sheer size—such as a nationally coordinated consolidation centered on the largest incumbents—tend to raise prices and harm consumers, delivering far smaller net benefits even when costs fall. As Nevo (2000) famously showed in the US cereal industry, mergers that increase market power without offsetting efficiency gains can leave consumers worse off, even if they appear profitable for the merging firms.

The real world merger wave falls short

Between 2018 and 2024, China saw a wave of steel mergers. We do not attempt to explain why these specific mergers occurred; they likely reflect a combination of government directives and institutional constraints among other factors and are treated as given. Our aim is instead to evaluate their welfare consequences against the benchmark of what better-designed consolidation could have achieved.

The study finds these actual deals captured less than a quarter of the potential welfare gains that could have been achieved under a well designed regional consolidation. The dominant player was Baowu Steel, a central state owned enterprise and the world’s largest steelmaker. While Baowu’s acquisitions delivered about 60% of the gains from all actual M&A, the overall outcome still fell far short of what was possible.

The gap between what was possible and what was achieved raises a deeper question: why did actual M&A fall so far short of the efficiency enhancing regional consolidation scenario? One interpretation is that the government’s approach—focused on creating national champions like Baowu—prioritized producer interests over consumer welfare. This tension between producer and consumer welfare echoes a broader theme in the literature on misallocation: Hsieh and Klenow (2009) famously showed that when capital is directed toward large but less productive firms—rather than toward the most efficient producers—the aggregate costs can be enormous, and poorly designed merger policy risks replicating the same distortion at an even larger scale. In the actual wave, prices did not fall, markups rose, and the gains went largely to producers rather than consumers. This suggests that industrial policy, even when it succeeds in raising efficiency, can still deliver disappointing results if it also expands market power in ways that hurt the buyers of steel.

Figure 2: Welfare gains under different merger designs. National mergers led by the largest firms—especially without cost savings—can reduce welfare. Regional mergers led by efficient firms generate the largest gains. The actual merger wave (2018–2024) achieved only a fraction of the welfare improvement possible under a well designed regional consolidation.

Shifting demand and the limits of supply side reform

The study also highlights a crucial but often overlooked factor: demand moves. Between 2017 and 2023, a slowdown in real estate—which accounts for 45% of steel consumption—reduced national steel demand by 3.6%. But the impact was wildly uneven across regions. In the Southwest, where firms sell mostly locally, the decline in demand was fully passed through to local producers. In the Northeast, which ships much of its steel to other regions, the local slowdown was partly cushioned.

This matters because the success of supply side reforms depends on how well supply can adjust to these spatial shifts in demand. As China’s economy evolves—with construction cooling and high tech manufacturing expanding—the geographic pattern of steel demand will continue to change. A merger policy that ignores geography will struggle to keep up.

Final thoughts

For a country that produces half the world’s steel, getting consolidation right is not just an industrial issue—it is a test of how well policy can balance efficiency, competition, and geography. The evidence points toward a more nuanced path: enabling the right firms, in the right places, to lead the industry’s transformation, rather than simply merging to maximise size.

References

Brandt, Loren, Feitao Jiang, Yao Luo, and Yingjun Su. 2026. “The Geography of Market Power: Evidence from the Chinese Steel Industry.” University of Toronto Department of Economics Working Paper No. 820. https://www.economics.utoronto.ca/public/workingPapers/tecipa-820.pdf.

Collard Wexler, Allan, and Jan De Loecker. 2015. “Reallocation and Technology: Evidence from the US Steel Industry.” American Economic Review 105 (1): 131–71. https://doi.org/10.1257/aer.20130090.

Hsieh, Chang-Tai, and Peter J. Klenow. 2009. “Misallocation and Manufacturing TFP in China and India.” Quarterly Journal of Economics 124 (4): 1403–48. https://doi.org/10.1162/qjec.2009.124.4.1403.

Miller, Nathan H., and Matthew Osborne. 2014. “Spatial Differentiation and Price Discrimination in the Cement Industry: Evidence from a Structural Model.” RAND Journal of Economics 45 (2): 221–47. https://doi.org/10.1111/1756-2171.12049.

Nevo, Aviv. 2000. “Mergers with Differentiated Products: The Case of the Ready to Eat Cereal Industry.” RAND Journal of Economics 31 (3): 395 421. https://doi.org/10.2307/2600994.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017