A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Contract Design and Insurance Take-up

Offering farmers a menu of insurance contracts instead of a single option significantly increases insurance take-up, by changing how farmers evaluate options within the contract menu.

Agricultural insurance is widely viewed as an important tool for helping farmers manage risk, yet insurance take-up remains persistently low in many settings. This is true even in environments where risks are substantial and insurance products are subsidized. Much of the existing discussion focuses on demand-side barriers: farmers may lack trust in insurers, have limited understanding of insurance products, or face liquidity constraints (Gaurav et al. 2011, Cole et al. 2013, Cai et al. 2015). However, insurance coverage often remains limited despite efforts to address these constraints.

This suggests that other factors may also play an important role. In particular, relatively little attention has been paid to supply-side features of insurance products themselves. In many programs, farmers are offered only a single contract with a fixed premium and payout structure. This approach simplifies administration but may not reflect the substantial heterogeneity across farmers in risk exposure, production scale, and willingness to pay. These observations raise a natural question: does insurance contract design affect farmers’ demand for insurance? Can offering a menu of contracts, rather than a single option, increase take-up?

The study: Offering menus of insurance contracts

To address those questions, we conducted a field experiment with rice farmers in China in collaboration with a local agricultural insurance provider. The provider’s standard product offers farmers a single insurance contract with a fixed premium and payout structure.

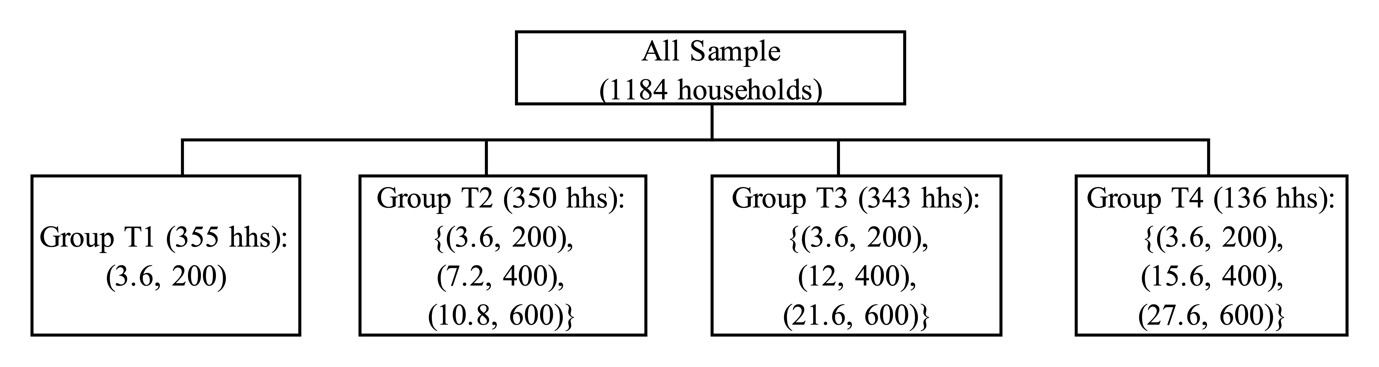

In our experiment, we varied the set of contracts offered to farmers. As shown in Figure 1, farmers were randomly assigned to one of two groups:

1. Single contract (Group T1): Farmers were offered only the standard contract, under which they pay a premium of 3.6 RMB for a maximum payout of 200 RMB per mu of rice production.

2. Contract menu (Groups T2–T4): Farmers were offered a menu of three contracts that differed in premiums and payouts. The menu included a basic contract with the lowest premium and payout, a moderate-coverage contract (maximum payout 400 RMB), and a high-coverage contract (maximum payout 600 RMB). Within this menu, we experimentally varied the relative prices across contracts, generating different menu configurations.

This design allowed us to examine whether expanding the set of contract options affects insurance take-up, and how farmers’ choices respond to relative price comparisons within the menu.

Figure 1. Experimental Design

Expanding the contract menu increases insurance take-up

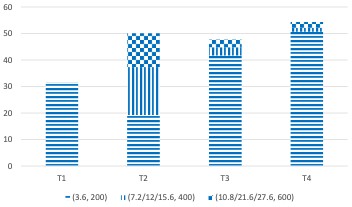

Our results show that expanding the contract menu substantially increases insurance take-up. As shown in Figure 2, introducing additional contract options increased overall insurance take-up from about 30% in Group T1 to roughly 50% in Groups T2, T3, and T4.

Interestingly, relative prices strongly affect which contract households choose. In Group T2, where the additional contracts were priced proportionally to the basic contract, take-up of the basic contract declined and a substantial share of households selected one of the higher-coverage options. By contrast, as the additional contracts became increasingly expensive relative to the basic contract (Groups T3 and T4), most of the increase in demand came from farmers choosing the basic contract with the lowest premium and payout. In other words, offering additional contract options encouraged more farmers to purchase insurance, even though many ultimately selected the same basic policy that was available when only one contract was offered.

Figure 2. Average Insurance Take-up Rates (%) by Contract Menu

Why does a menu increase demand?

Why does expanding the contract menu increase insurance take-up? One explanation is a context effect, whereby choices depend on the presence and characteristics of other available options. In this setting, introducing more expensive alternatives may increase the relative attractiveness of the basic contract, leading to higher take-up. A second explanation is information inference: farmers may update their beliefs based on the contract set itself. For example, variation in premiums and payouts may convey information about disaster risk. In addition, offering multiple contract options may signal that the insurance program is more carefully designed or more reliable, thereby improving perceived product quality.

To distinguish between these mechanisms, we separately randomized whether households received explicit information about the existence of alternative contracts and the historical probability of weather-related disasters. This design allowed us to isolate the role of relative price comparisons from belief updating.

The results show that the effect of contract menus is not driven by information inference. The information intervention significantly increased farmers’ knowledge about the insurance program—including awareness of alternative contract options and understanding of disaster risk—indicating that the treatment is effective. However, despite this increase in knowledge, providing explicit information did not affect insurance take-up and did not attenuate the impact of contract menus.

Conclusion and policy implications

Our findings have direct implications for the design and scale-up of insurance programs. Much of the policy discussion around low insurance take-up has focused on demand-side interventions, such as insurance education, information campaigns, and subsidies. Our results highlight the importance of supply-side design choices.

We find that contract menu design affects insurance demand in two main ways. First, when higher-coverage contracts are offered at comparable prices, households shift toward these options, consistent with improved matching between contract features and heterogeneous preferences. Second, and more surprisingly, offering additional—especially more expensive—contracts can increase take-up of the basic plan. Rather than shifting demand toward higher coverage, expanding the menu can make the basic contract more attractive by changing how households compare available options.

These two patterns have distinct policy implications. When more generous contracts are offered at similar prices, providing multiple options allows households to select coverage that better fits their needs, increasing participation through improved matching. When budget constraints limit subsidies for higher coverage, expanding the contract menu can still increase participation by leveraging comparison effects that make the basic contract more attractive. In this way, contract menu design offers a flexible and cost-effective supply-side approach to expanding insurance coverage across different fiscal environments. More broadly, the findings highlight that improving financial inclusion may depend not only on reducing barriers to access, but also on designing financial products in ways that better align with how people make decisions.

References

Cai, Jing, Alain de Janvry, and Elisabeth Sadoulet. 2015. “Social Networks and the Decision to Insure.” American Economic Journal: Applied Economics 7 (2): 81–108. https://doi.org/10.1257/app.20130442.

Cai, Jing. 2026. “Contract Design and Insurance Demand.” National Bureau of Economic Research Working Paper No. 34797. https://www.nber.org/papers/w34797.

Cole, Shawn, Xavier Giné, Jeremy Tobacman, Petia Topalova, Robert Townsend, and James Vickery. 2013. “Barriers to Household Risk Management: Evidence from India.” American Economic Journal: Applied Economics 5 (1): 104–35. https://doi.org/10.1257/app.5.1.104.

Gaurav, Sarthak, Shawn Cole, and Jeremy Tobacman. 2011. “Marketing Complex Financial Products in Emerging Markets: Evidence from Rainfall Insurance in India.” Journal of Marketing Research 48 (SPL): 150–62. https://doi.org/10.1509/jmkr.48.SPL.S150.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017