A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Trading Suspensions, Liquidity, and Information Acquisition in the Chinese Stock Market

We study the implications of mutual fund liquidity creation by examining frequent trading suspensions in China, which eliminate market liquidity in affected stocks and cause significant mispricing of mutual funds due to inaccurate valuations of their illiquid holdings. Investors actively acquire information about suspended stocks held by mutual funds, driving flows into underpriced funds. This information is subsequently incorporated into stock prices when trading resumes, suggesting that mutual fund liquidity creation stimulates information acquisition about illiquid, information-sensitive assets.

Stock trading suspensions and price movements at resumption

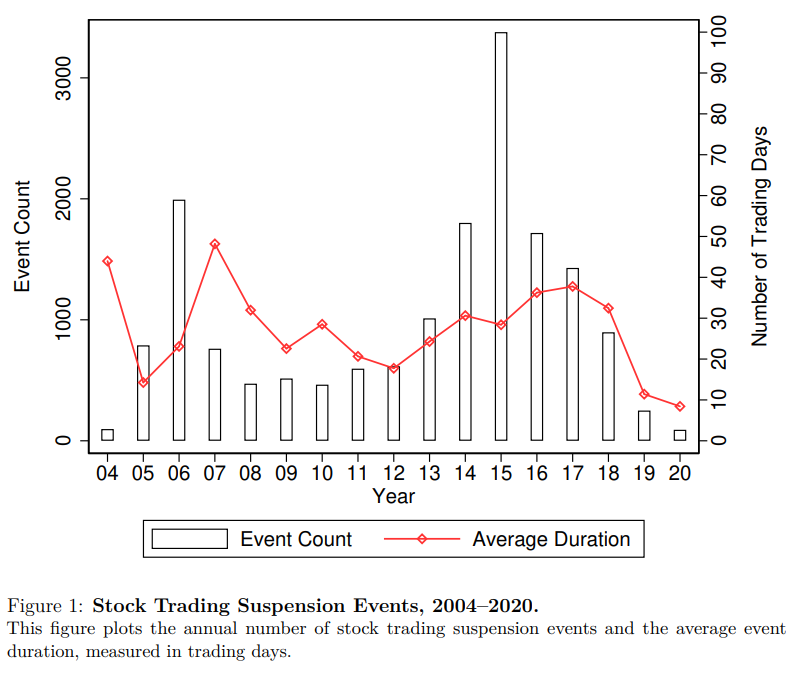

Trading suspensions on individual securities are a pervasive institutional feature of many emerging markets, particularly in China. The two exchanges, the Shanghai Stock Exchange and the Shenzhen Stock Exchange, both allow publicly listed firms to suspend trading before major corporate events. Firms may request suspensions when planning major events such as asset acquisitions, mergers, and restructurings. Historically, these requests were often granted with limited regulatory scrutiny. Between 2004 and 2020, there were 16,958 multiday trading suspensions, affecting nearly 80% of public firms at least once. At any point in time, on average 4.6% of stocks were suspended. As Figure 1 shows, typically 500–2,000 suspensions occur per year, with durations ranging from 30 to 50 trading days, though some persist for many months. Despite the prevalence of these prolonged trading interruptions and frequent media coverage, relatively little is known about how investors respond to them, or what these responses imply for broader theories of information, liquidity, and financial intermediation.

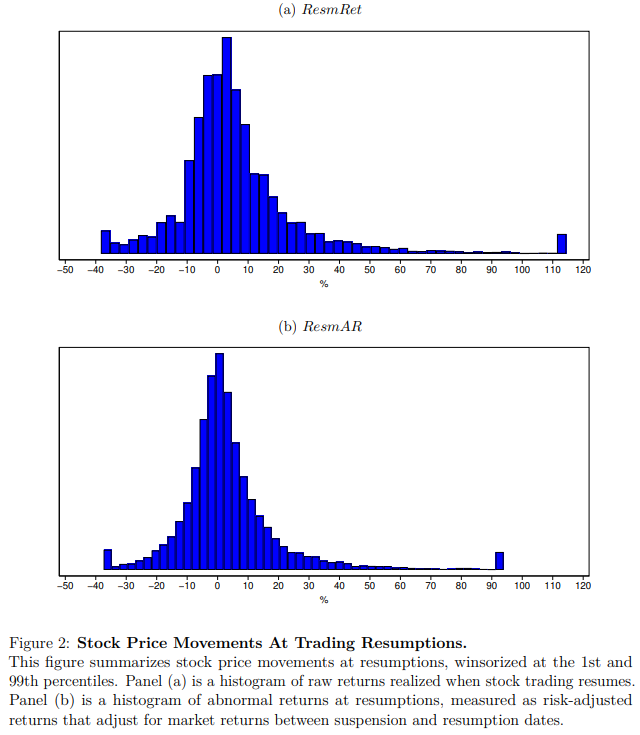

When a stock is suspended, its market liquidity is largely eliminated, and value-relevant information can no longer be incorporated into the stock’s price. Once trading eventually resumes, the accumulated information is rapidly incorporated into the stock’s price, often causing a large price jump. Indeed, Chinese stocks often exhibit large, firm-specific price movements upon trading resumptions, reflecting the information observed by investors during the illiquidity period. Figure 2 presents the distribution of stock price movements at resumptions. The magnitude of these positive and negative returns remains large even after excluding stock market returns realized during the suspension period, suggesting important post-resumption price discovery in the Chinese stock market.

Mutual funds as liquidity providers for illiquid assets

In modern financial systems, a large sector of financial intermediaries—mutual funds—creates liquidity by allowing investors to indirectly invest in illiquid assets. China is no exception: thousands of mutual funds are available to investors, offering liquid shares that can be purchased or redeemed daily at net asset values (NAVs). Many of these mutual funds hold suspended stocks in their portfolios, often with significant portfolio weights. As a result, even when a stock is non-tradable, investors can still gain exposure to it indirectly by trading mutual fund shares, which act as an alternative liquidity channel for illiquid assets.

What happens when mutual funds hold suspended stocks? Traditional theories of financial intermediation focus on how intermediaries create liquidity using debt claims such as bank deposits (Diamond and Dybvig 1983, Gorton and Pennacchi 1990). As debt is information-insensitive, this liquidity discourages investors from acquiring information about the underlying assets (Dang et al. 2017). However, unlike banks, mutual funds create liquidity with equity shares (Chernenko and Sunderam 2016, Ma et al. 2025). The value of mutual fund shares is sensitive to information about suspended stock holdings, and their NAVs are susceptible to mispricing if such information is not reflected in stock valuations. As a result, mutual funds may encourage investor information-gathering when they hold hard-to-price, illiquid assets with significant weights.

NAV mispricing from suspended stock holdings

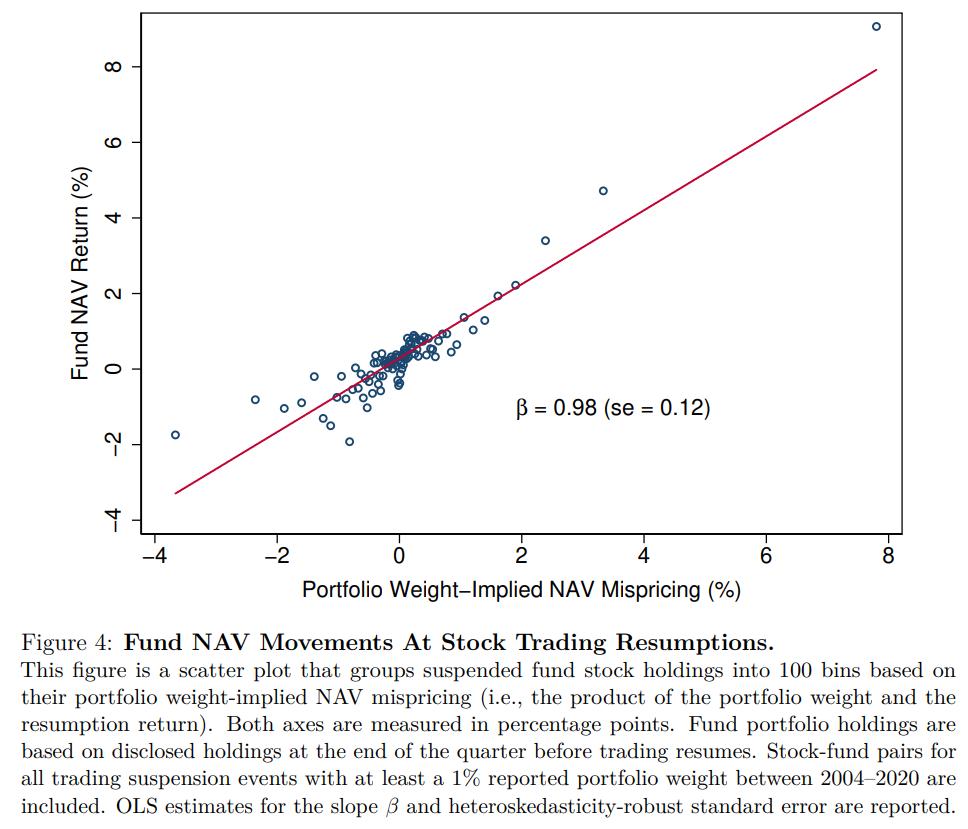

Our study documents that mutual funds frequently hold large positions in suspended stocks, and these illiquid holdings lead to pervasive and significant NAV mispricing. Fund companies often fail to adequately adjust their valuations for suspended stocks, so the fund’s reported NAV drifts away from the stock’s fundamental value during the suspension. Once stock trading resumes, the fund’s NAV experiences a correction as the previously stale-priced stock holding is marked to market. Figure 4 plots the fund’s NAV return at resumption against the suspended stock’s portfolio weight-implied mispricing. There is an almost one-for-one relationship between the weight-implied mispricing and the actual fund NAV return, indicating a predictable NAV correction when trading resumes. The mutual fund’s liquidity thus allows investors to exploit this mispricing using firm-specific information.

Investor flows and “arbitrage via mutual funds”

The information-sensitivity of mutual fund shares attracts sophisticated investors. Our findings show that these investors actively exploit funds holding underpriced suspended stocks—a practice frequently described as “arbitrage via mutual funds” in Chinese financial media. Specifically, we observe significant capital flows into mutual funds with underpriced NAVs before their suspended holdings resume trading, aiming to capture the NAV rebound. The flow response is sizable: on average, a 1% NAV mispricing attracts quarterly flows amounting to 3% of the fund’s total assets, which dilutes the return of long-term fund investors. This response is stronger for fund shares held by institutional investors and is primarily driven by inflows into underpriced funds, since short-selling fund shares is not possible. We also observe increased discussions about specific funds’ suspended holdings in Eastmoney, a popular Chinese internet mutual fund forum. These activities occur only when the suspended holdings are disclosed to investors before trading resumes, supporting the interpretation that it is information about suspended holdings that drives the flows.

Information acquisition during suspensions

Ex ante, the liquidity created by mutual funds makes the information about suspended stocks actionable and thus more valuable to investors: even if they cannot directly use this information in stock trading, they can use it to better predict fund NAVs when stock trading resumes and profit from these predictive NAV movements. Consistent with this idea, we find that stocks with greater exposure to mutual funds (i.e., those held with larger weights by funds) experience more intensive information acquisition by investors during the suspension. This effect manifests in the acquisition of both private information (through on-site corporate visits by investment professionals) and public information (through internet search queries about the firm).

Enhanced stock price informativeness at resumption

The information acquisition induced by mutual fund liquidity does not end with investors’ trading of fund shares; it ultimately affects the suspended stock’s price when it resumes trading. Because firms with greater mutual fund exposure were analyzed by investors during suspensions, their stocks exhibit more informative price movements when liquidity comes back at trading resumption. Empirically, we find that stocks with higher portfolio weights in mutual funds tend to have larger post-resumption price movements, suggesting more information being impounded into prices. Moreover, those price movements are also better linked to the firm’s subsequent earnings surprises.

Conclusion

Our study uncovers a novel channel whereby mutual fund liquidity creation stimulates investor information acquisition about illiquid, information-sensitive assets. This insight highlights an important role of modern nonbank intermediaries: by offering liquidity in illiquid assets, they serve as a catalyst of information and enhance price discovery, making asset prices more informative about fundamental values. However, this role also has a flip side. The information about illiquid holdings causes value transfers between fund investors with different levels of sophistication. In extreme cases, it can potentially trigger fund runs, a risk that regulators may need to manage through fund valuation, disclosure, or redemption rules. Overall, our findings point to the need for a prudential regulatory framework for securities trading and fund valuation that addresses the growing importance of intermediaries offering liquidity transformation.

References

Chernenko, Sergey, and Adi Sunderam. 2016. “Liquidity Transformation in Asset Management: Evidence from the Cash Holdings of Mutual Funds.” National Bureau of Economic Research Working Paper No. 22391. https://www.nber.org/papers/w22391.

Dang, Tri Vi, Gary Gorton, Bengt Holmström, and Guillermo Ordoñez. 2017. “Banks as Secret Keepers.” American Economic Review 107 (4): 1005–29. https://doi.org/10.1257/aer.20140782.

Diamond, Douglas W., and Philip H. Dybvig. 1983. “Bank Runs, Deposit Insurance, and Liquidity.” Journal of Political Economy 91 (3), 401–19. https://doi.org/10.1086/261155.

Gorton, Gary, and George Pennacchi. 1990. “Financial Intermediaries and Liquidity Creation.” Journal of Finance 45 (1): 49–71. https://doi.org/10.2307/2328809.

Ma, Yiming, Kairong Xiao, and Yao Zeng. 2025. “Bank Debt, Mutual Fund Equity, and Swing Pricing in Liquidity Provision.” National Bureau of Economic Research Working Paper No. 33472. https://www.nber.org/papers/w33472.

Sialm, Clemens, and David X. Xu. 2026. “Trading Suspensions, Liquidity, and Information Acquisition in the Chinese Stock Market.” Forthcoming.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017