A Bridge on Economic Issues between China and the World

Facebook

Facebook  Twitter

Twitter  Instagram

Instagram WeChat

WeChat  Email

Email Impacts of Housing Policy: China’s Experiment

China’s unprecedented and unexpected loosening of loan-to-value ratio (LTV) policy during 2014Q4–2016Q3 provides an ideal case to study the role of housing policy in housing booms and busts and its impacts on consumption and debt burdens among households. Evidence from three unique micro datasets shows that such a policy change disproportionately increased the share of mortgages to middle-aged and high-income homeowners in the total amount of newly issued mortgages and at the same time reduced their consumption growth persistently. Homeowners traded up their primary homes as their speculative housing investment. This trade-up was a key channel for a change in LTV policy to exert aggregate and distributional impacts on mortgage markets.

The COVID-19 pandemic in 2020 propelled the world into a deep recession. In China, however, the duration of this recession was transient, and recovery was driven by rapid growth of sales of residential properties since May 2020. In August 2020, the year-over-year nationwide growth rate peaked at 30%, making real estate a bright spot of growth and recovery. In first-tier cities like Shenzhen and Shanghai, there has been a new fever in the market for newly built properties. This housing boom caused policymakers to tighten regulations on the housing market during the second half of 2020. What is the role of housing policy in housing booms and busts? How do housing regulations affect consumption and debt burdens across households? Researchers have explored many issues related to the real estate market from both empirical and theoretical perspectives (see, for example, Fang, Gu, Xiong, and Zhou 2015; Wu, Gyourko, and Deng 2016; Glaeser, Huang, Ma, and Shleifer 2016; Chen and Wen 2017; and Chen, Liu, Xiong, and Zhou 2019. The impacts of housing policy on the real estate market and household finances, however, are an important topic that is largely unexplored, partly because there are no large changes in housing policy observed in many countries and partly because there is a lack of comprehensive data on how households finance their mortgages and consumption.

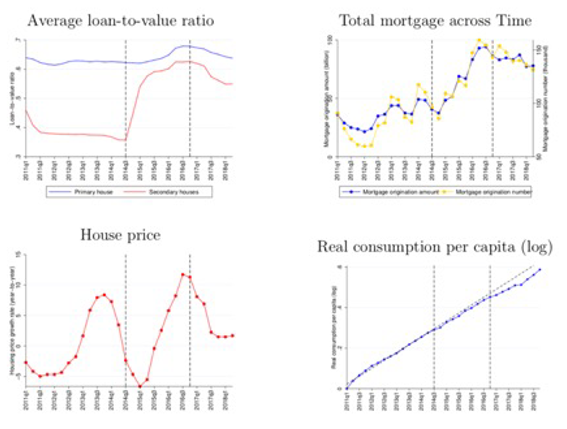

In Chen, Wang, Xu, and Zha (2020), we use China’s loan-to-value ratio (LTV) policy and in particular a relaxation of this policy during 2014Q4–2016Q3 as a case study to address the aforementioned questions. LTV policy was changed by an unprecedented and unexpected reduction in the minimum down payment ratio of non-primary houses from 60–70% to 30%. The intent of this policy was to resolve overstocked housing markets created by China’s monetary and fiscal stimulus in 2009. During this period, however, the annualized growth rate of real house prices across 70 major Chinese cities was, on average, 5.94% higher than in 2011Q1–2014Q3 (for first-tier and second-tier cities, it was 8.84% higher), and the average annual newly issued mortgage amount for these cities was 92% higher than in 2013. Meanwhile, the growth rate of aggregate consumption has declined since 2014Q4, and the decline continued even after the loosening of LTV policy was reversed in 2016Q4 (Figure 1).

Figure 1: LTV Policy Relaxation and Mortgage Boom

Source: Chen, Wang, Xu, and Zha (2020)

We exploit three unique micro datasets: a proprietary loan-level dataset for mortgage originations in one of the largest Chinese commercial banks, the China Household Finance Survey conducted by Southwestern University of Finance and Economics, and monthly city-level consumption data from China UnionPay Merchant Services Corporation. A combination of these datasets enables us to establish the following key findings:

(1) the loosening of LTV policy for non-primary houses fueled the entire mortgage boom during 2014Q4–2016Q3;

(2) the mortgage expansion disproportionately increased the share of mortgages to middle-aged and high-education homeowners in total newly issued mortgages (in terms of both the amount and the number of originations), while their consumption growth declined persistently;

(3) and homeowners traded up their primary homes as speculative housing investment—a key channel for a change in LTV policy to exert aggregate and distributional impacts on mortgage markets.

LTV Policy and Mortgage Boom

To study how a relaxation of LTV policy during 2014Q4–2016Q3 drove mortgage demands of households of different ages and income levels, we exploit proprietary mortgage loan level data from one of the largest banks in China, which covers all mortgage loans for purchasing new residential properties between 2011Q1 and 2018Q2. During the LTV policy relaxation period, middle-aged households with high education were the only age-education group whose mortgage share increased substantially, by 13.32% in the loan amount and 8.07% in the number of originations. By contrast, the mortgage share of other age-education groups declined substantially. Although the maximum LTV ratio barely changed for primary houses during this period, this reallocation was mainly driven by reallocation of mortgage credit to primary houses. This reallocation led to a significant increase in the ratio of mortgage debt to income for households who had outstanding mortgage debt prior to the housing boom (intensive margin) and a high mortgage participation rate (extensive margin), as shown in Figure 2.

Figure 2: Mortgage Debt Burdens

Source: Chen, Wang, Xu, and Zha (2020)

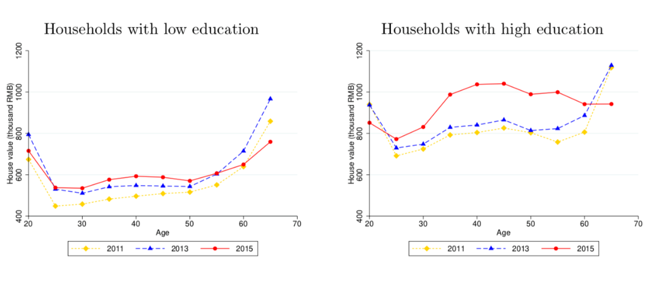

The main reason for a significant increase of the mortgage share of middle-aged households with high education is that homeowners traded up their existing homes for larger or better-quality houses. Between 2013 and 2015, after controlling for house price increases, the average house value for households of age 30–55 with high education increased by about 20% (Figure 3). There was no such increase for households of other ages or those with low education.

Figure 3: Average House Values: Primary Homes

Source: Chen, Wang, Xu, and Zha (2020)

Most homeowners in this middle-aged and high-education group did not purchase secondary houses. The intended policy shock on secondary houses, therefore, had indirect impacts on the market of primary homes, as the initial increase in the house price driven by an increase in demands for secondary houses generated capital gains for existing homeowners and encouraged them to trade up existing primary homes in anticipation of further capital gains in the future. These indirect (and unintended) impacts, facilitated by the speculation of higher house prices in the future, turned out to be a major driving force of the mortgage boom in response to the change of LTV policy.

Consumption Growth and Mortgage Debt Burdens

To assess empirically the impacts of the mortgage boom on consumption growth, we use biannual China Household Finance Surveys from 2011 to 2017. There are three key empirical findings.

First, the only age-education group that experienced a significant decline in consumption growth between two sample periods (2013–2015 and 2015–2017) is middle-aged households with high education. Despite faster income growth in 2015–2017, these households experienced a significant decline in consumption growth, by 3.59% per annum.

Second, within this age-education group, consumption growth of homeowners fell by 3.61% even though their incomes increased by 5.25%, while there was no evidence of a decline in consumption for renters.

Third, there is a causal relationship between homeowners’ mortgage debt burden and their consumption growth. After controlling for age, education, and family size, our estimation reveals that households with mortgage debt had, on average, slower consumption growth than households with no mortgage debt by 2.66%. If households’ outstanding mortgage debt increased by 1% over their incomes, their consumption growth rate would fall by 0.27%. All these empirical findings imply that an increase in the mortgage share of middle-aged households with high education contributed to a significant slowdown of their consumption, because these households were more financially constrained by their mortgage debt.

Cross-City Evidence on Housing Speculations

Much of the increase in mortgage demands and the decline in consumption growth among middle-aged homeowners with high education was due to speculation on the return of housing investment. To establish this evidence, we exploit cross-city variations in their exposures to housing speculations. Following Gao, Sockin, and Xiong (2020), we measure a city’s exposure to housing speculation by the share of mortgages to non-primary houses in all mortgages in 2013, the year prior to the loosening of LTV policy. During the period of loose LTV policy, cities with high exposure experienced more rapid increases in their house prices, total mortgages, and the mortgage share of middle-aged households with high education than cities with low exposures. These differences diminished after the relaxation of LTV policy was reversed.

Consumption in high-exposure cities decreased steadily relative to consumption in low-exposure cities during the period when LTV policy was relaxed and continued to decline even after the policy relaxation ended. This city-level evidence supports a theory that housing speculation played a key role in fueling the mortgage boom and at the same time reducing non-housing consumption during 2014Q4–2016Q3 when LTV policy was drastically loosened.

A Theoretical Explanation

All these empirical findings can be explained by a life-cycle equilibrium model with heterogeneous households. The model uncovers a self-reinforcing mechanism via changes in the house price: a reduction of the minimum down payment ratio for secondary houses triggers an initial rise in the house price by encouraging investment in houses for speculative purposes; the initial rise, in turn, generates capital gains for existing homeowners and encourages them to trade up existing homes in anticipation of future capital gains. Growth of non-housing consumption of middle-aged households with high incomes falls partly because of their intertemporal substitution into future consumption and partly because of the increasing burden of mortgage debt relative to income. This self-reinforcing mechanism is in sharp contrast to the standard mechanism in other models in the literature. In those models, changes in credit conditions affect aggregate housing demands mainly through housing tenure decisions made by households who are credit constrained for housing services, not for housing investment.

Conclusion

The loosening of LTV policy during 2014Q4–2016Q3 and the resultant mortgage boom, although transitory, had persistent effects on the slowdown of consumption because the rising mortgage debt burdens were born by middle-aged and high-income homeowners. Recent developments in China bear witness to the valuable lesson we have learned from China’s 2014Q4–2016Q3 experiment. Total retail sales of consumer goods for the first 11 months of 2020 declined by 4.8% from the same period the previous year, while home building increased by 7% for the same period. To promote growth of household consumption, policymakers should be mindful of the crowding-out effects of rising house prices and rising mortgage debts on a wide class of homeowners.

With continuing urbanization while financial markets are still underdeveloped, speculative investment in houses will likely be an important driver of households’ housing demands, despite various administrative means to contain such demands. In its fourteenth five-year plan of national economic and social developments, the Chinese government has stated that one of its long-term goals is to boost domestic consumption as a lever for the development of the whole economy. Against this backdrop, future housing policy for regulating the housing markets should take into account households’ expectations of the profitability of housing investment and how these expectations would negatively affect consumption growth.

The views expressed herein are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Atlanta or the Federal Reserve System.

(Kaiji Chen, Economics Department, Emory University and Federal Reserve Bank of Atlanta; Qing Wang, Institute of Chinese Financial Studies, Southwestern University of Finance and Economics; Tong Xu, Institute of Chinese Financial Studies, Southwestern University of Finance and Economics; Tao Zha, Federal Reserve Bank of Atlanta and Emory University.)

References

Chen, Kaiji and Yi Wen. 2017. “The Great Housing Boom of China.” American Economic Journal 9 (2): 73-114. https://www.aeaweb.org/articles?id=10.1257/mac.20140234.

Chen, Kaiji, Qing Wang, Tong Xu, and Tao Zha. 2020. “Aggregate and Distributional Impacts of LTV Policy: Evidence from China’s Micro Data.” NBER Working Paper 28092. https://www.nber.org/system/files/working_papers/w28092/w28092.pdf.

Chen, Ting, Laura Xiaolei Liu, Wei Xiong, and Li-An Zhou. 2019. “Real Estate Boom and Misallocation of Capital in China.” Unpublished manuscript. http://cicm.pbcsf.tsinghua.edu.cn/Public/Uploads/upload/CICM2019-67.pdf.

Fang, Hanming, Quanlin Gu, Wei Xiong, and Li-An Zhou. 2016. “Demystifying the Chinese Housing Boom.” In NBER Macroeconomics Annual, edited by Martin Eichenbaum and Jonathan A. Parker, 105–66. Chicago: University of Chicago Press. https://doi.org/10.1086/685953” https://doi.org/10.1086/685953.

Gao, Zhenyu, Michael Sockin, and Wei Xiong. 2020. “Economic Consequences of Housing Speculation.” Review of Financial Studies 33 (11): 5248–87. https://doi.org/10.1093/rfs/hhaa030.

Glaeser, Edward, Wei Huang, Yueran Ma, and Andrei Shleifer. 2016. “A Real Estate Boom with Chinese Characteristics.” Journal of Economic Perspectives 31 (1), 93–116. https://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.31.1.93.

Wu, Jing, Joseph Gyourko, and Yongheng Deng. 2016. “Evaluating the Risk of Chinese Housing Markets: What We Know and What We Need to Know.” China Economic Review 39 (July 2016), 91–114. https://doi.org/10.1016/j.chieco.2016.03.008.

Latest

Most Popular

- VoxChina Covid-19 Forum (Second Edition): China’s Post-Lockdown Economic Recovery VoxChina, Apr 18, 2020

- China’s Great Housing Boom Kaiji Chen, Yi Wen, Oct 11, 2017

- China’s Joint Venture Policy and the International Transfer of Technology Kun Jiang, Wolfgang Keller, Larry D. Qiu, William Ridley, Feb 06, 2019

- The Dark Side of the Chinese Fiscal Stimulus: Evidence from Local Government Debt Yi Huang, Marco Pagano, Ugo Panizza, Jun 28, 2017

- Wealth Redistribution in the Chinese Stock Market: the Role of Bubbles and Crashes Li An, Jiangze Bian, Dong Lou, Donghui Shi, Jul 01, 2020

- Evaluating Risk across Chinese Housing Markets Yongheng Deng, Joseph Gyourko, Jing Wu, Aug 02, 2017

- What Is Special about China’s Housing Boom? Edward L. Glaeser, Wei Huang, Yueran Ma, Andrei Shleifer, Jun 20, 2017

- Privatization and Productivity in China Yuyu Chen, Mitsuru Igami, Masayuki Sawada, Mo Xiao, Jan 31, 2018

- Daily Price Limits and the Magnet Effect Ting Chen, Zhenyu Gao, Jibao He, Wenxi Jiang, Wei Xiong, Oct 25, 2017

- How did China Move Up the Global Value Chains? Hiau Looi Kee, Heiwai Tang, Aug 30, 2017